|

| Source |

The key message of the graph is the contrast between the 5-year straight-line depreciation and the curves showing the value of the remaining Bitcoin that the rig will generate. I suggested that the same mismatch between straight-line depreciation and remaining value generation would apply to AI hardware. I don't claim to be the first to flag this issue; The Economist's The $4trn accounting puzzle at the heart of the AI cloud was about a month earlier.

About a month later I returned to AI economics with Mind The GAAP, but that was mostly focused on other parts of the puzzle.But now, thanks to Bryce Elder's Big tech’s $680bn buy-now-book-later problem it turns out that both Michael Burry of The Big Short and Morgan Stanley Research agree with me that there's a problem:

Below the fold I go into the details, with many thanks to Bryce Elder.

|

| Source |

{kind=link}

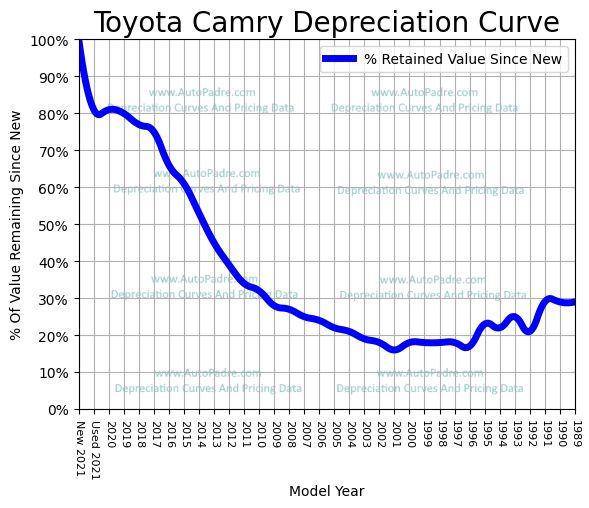

would unveil a fresh AI chip every year rather than every couple of years. In March its boss, Jensen Huang, remarked that “when Blackwell starts shipping in volume, you couldn’t give Hoppers away,” referring to Nvidia’s latest chips and their predecessors, respectively.Second, Camry depreciation is a curve, not a straight line, and it retains a small proportion of its initial value for a long time. This is similar to what happens to mining rigs, which are often deployed in shipping containers so that, as they become uneconomic in areas of relatively high power costs, they can be shipped to areas with cheaper power to extend their life. We haven't seen this yet with Nvidia racks, which have much more demanding environmental requirements.

Right now older hardware can still make money; because the AI frenzy means AI hardware is supply-limited people can't get the newer hardware that would make much more money. Michael Burry makes this point:

The idea of a useful life for depreciation being longer because chips from more than 3-4 years ago are fully booked confuses physical utilization with value creation. Just because something is used does not mean it is profitable. GAAP refers to economic benefits.But projecting this value for older hardware into the future involves assuming the supply constraint will continue indefinitely. Once supply constraints lessen the value they create for older hardware will vanish.

Airlines keep old planes around for overflow during Thanksgiving or Christmas, but are only marginally profitable on the planes all the same, and not worth much at all.

|

| Source |

Internet companies are in denial about getting fat. The advertising silos and data miners of 10 years ago are now infrastructure-heavy and capital-intensive, but their reporting has yet to adjust to the rapid weight gain.

This mismatch may become harder to ignore as the value of their spending is written off. Morgan Stanley forecasts that, collectively, Microsoft, Oracle, Meta Platforms and Alphabet could book more than $680bn in depreciation charges over the next four years

|

| Source |

Hyperscalers have since 2020 been lengthening the assumed useful lives for their servers and network equipment, with only Amazon in 2025 going the other way. The ... chart simplifies things but shows the general direction of travel:

|

| Source |

Understating depreciation by extending useful life of assets artificially boosts earnings -one of the more common frauds of the modern era.The boost to earnings can be significant:

Though depreciation is a non-cash cost, the money having already been spent, any change to useful life assumptions has a big effect on GAAP income. For example, Google owner Alphabet raised earnings guidance in 2023 by $3bn by increasing the longevity of data centre equipment by a year or two.Depreciation is applied through time. What matters isn't just the rate, but also whet it starts:

The value of a data centre under construction is held on a company’s balance sheet, but depreciation is only being applied after it becomes operational. Data centres take years to build, so the delay between a capital outlay and a net income deduction can be very long.

Also: capex adds to a company's book value, showing up immediately in the cash flow statement as investments in property, plant and equipment, without a parallel increase in depreciation expense on the income statement. Comparing the former with the latter will exaggerate average asset longevity.

|

| Source |

Elder is using estimate compiled by Morgan Stanley’s Accounting & Tax desk:

The team splits hyperscaler capex into AI and non AI, smooths out construction-in-progress costs, and allocates the expected lease expenses to property. The team assumes GPUs have a useful life of up to six years and that warehouses will last for 15 years.These assumptions are very generous to the hyperscalers:

- Even if we discount Nvidia's plan to switch to a one-year cadence, they assume GPUs more than two generations obsolete can generate enough income to pay for their power, cooling and space.

- The idea that the physical data center will accomodate 7 generations of racks is laughable in light of the fact that the data centers currently being built are unlikely to accomodate the next major generation of Nvidia racks. How to design a data center that will is currently a research problem.

|

| Source |

Based on Morgan Stanley’s calculations, Alphabet’s depreciation expense could quadruple by its 2028 year-end. Oracle’s 2025 depreciation charge of $4bn might balloon to $56bn by 2029, which would be equivalent to 28 per cent of revenue expected by the consensus:It also looms large as a percentage of total expenses by 2029, with ORCL about 42%, META around 35%, MSFT around 32% and GOOG around 15%. Elder writes:

Those sorts of numbers challenge The Street’s assumption that, with the exception of Oracle, hyperscaler operating margins will improve over the next four years.

To gauge the potential hit to profitability, Morgan Stanley compares consensus revenue forecasts against operating expenses excluding depreciation. Its figures suggest that, to deliver what’s expected, hyperscaler costs ex depreciation need to collapse:

|

| Source |

Elder adds to the skepticism:

So far, hyperscaler costs have been doing the opposite of collapsing. Meta said overnight that its total expenses would be up to 44 per cent higher this year at between $162bn and $169bn, and that 2026 capex would be higher by up to 94 per cent at between $115bn and $135bn. Microsoft also raised capex materially, saying it intends to “roughly double our total datacenter footprint over the next two years”.So much for the hyperscalers' accounting problems. The pure-play AI companies have it even worse.

The biggest of the pure-play AI companies is OpenAI. How much revenue how soon do they need? Gareth Gore reports on that in OpenAI faces financial crunch point as huge supplier bills start to come due:

More than US$80bn of deferred commitments are set to come due this year, according to bank projections – including some linked to a deal last year to purchase US$250bn of compute from Microsoft.With a British level of understatement, Gore writes:

With other contracts that OpenAI has taken out with data centres, cloud computing providers and chip manufacturers over the past few years also starting to come due, the company is facing a wall of payment demands that could amount to several hundred billion dollars between now and the end of 2030.

How a company with just US$20bn in revenues pays for that is the big question. Larger rivals like Alphabet and Meta have legacy businesses generating hundreds of billions of dollars a year that they can draw on. OpenAI, by contrast, can only survive for as long as its backers are willing to keep it afloat.

“These are very important questions right now,” said Gil Luria, head of technology research at West Coast boutique investment bank DA Davidson. “If OpenAI can’t raise the capital it needs, that will cement the fact that the only big winners from AI will be the largest mega caps.”

|

| Source |

The $80B coming due this year would consume the $41B of the last capital raise plus twice last year's revenue. How is the capital raising going?:

“OpenAI was only able to raise capital primarily from one investor – SoftBank – during its last fundraise, which is one signal that there are not a lot of investors that are willing to participate at this size,” said Luria, who added that hopes of Gulf money are “a supposition at this point”.In OpenAI’s Insane Scaling Problem Will Lockett applies some skepticism to OpenAI's claim that "its Annualised Recurring Revenue (ARR) for 2025 was $20 billion.:

OpenAI has reported that ChatGPT had 800 million weekly users by the end of 2025. Multiple third-party sources have found that only 5% of users pay for ChatGPT, so we know that roughly 40 million people do. If they all pay the $20 per month subscription, that equates to $9.6 billion a year in revenue. But we also know that roughly 30% of OpenAI’s revenue comes from other sources, like licensing. So we can infer that the current annualised revenue should be around $13.7 billion. However, ChatGPT started 2025 with far fewer weekly users, which means that its total revenue for 2025 should be substantially below $13.7 billion.Lockett's suspicion is that it came from Microsoft:

This is why I personally find that $20 billion figure hard to believe. It looks like $10 billion or more has magically dropped into OpenAI’s wallet at some point in the last quarter of 2025. Where did that come from?

Integrating Copilot into essential subscriptions and services achieves two things. Firstly, it forces this terrible technology onto us, the public, which makes their numbers look better. And secondly, it means that Microsoft can technically claim that AI drives all the revenue generated from these subscriptions and services. As such, they could send 20% of it to OpenAI, even though their models didn’t directly create this revenue.Microsoft is reportedly starting to realize that forcing "this terrible technology onto us" is causing their customers to consider fleeing from Windows 11 to Linux. So why would they ship billions to OpenAI?

I suspect this is where that $10 billion-plus figure appeared from. OpenAI desperately needed cash, and Microsoft used this method to send it over covertly.

Lockett's answer is that Microsoft and OpenAI are in a partnership and OpenAI is desperate for cash:

Multiple analyses have found that OpenAI’s operational costs will be significantly more than $28 billion in 2025. So, even with $20 billion in revenue, they are still likely miles away from breaking even, let alone creating sustainable profit.Lockett posits that the reason OpenAI desperately needs cash is that they lack economies of scale:

...

Therefore, in the best-case scenario, where this $20 billion figure is honest revenue and OpenAI’s operational costs were as predicted, they would make an $8 billion loss in 2025. That is noticeably larger than the $5 billion loss they posted in 2024. But in the worst-case scenario, where their actual revenue is closer to $10 billion and their compute costs are accurately disclosed, they might face losses in the multiple tens of billions of dollars.

...

Regarding that $5 billion loss in 2024, it was actually large enough to threaten OpenAI with bankruptcy. In fact, the only reason OpenAI survived to see 2025 was due to a $6 billion corporate bailout from its backers, mainly Microsoft. Microsoft had sunk tens of billions of dollars into OpenAI and had already begun basing much of its new direction on its partnership with OpenAI. In other words, if OpenAI went under, it would be disastrous for Microsoft. Bailing them out was likely the cheaper option, even if it damaged OpenAI’s reputation.

But LLM AIs do not follow this trend. Scale does not reduce the unit cost. Furthermore, the cost of developing these AIs is increasing exponentially as they attempt to make them more capable (read more here). So, trying to give AI a larger scale (i.e., making it useful in more areas) can dramatically increase the unit cost.Les Barclays' Who Captures the Value When AI Inference Becomes Cheap? is a long, detailed discussion of the economics of AI. He notes that:

In other words, the larger and better you try to make AI, the further away from profitability it becomes, given that costs scale up faster than revenue.

OpenAI is proving this rather beautifully. Even if they have genuinely more than doubled their annual income from 2024, which I highly doubt, their annual loss has grown by at least 33%. They are going backwards, even further into the red. You can only do that for so long before the lights are turned off.

So this means the cost per query may be increasing for frontier models even as the cost per token declines which then creates a dynamic whereby improving technology makes AI economics more challenging, defying traditional business logic. AI companies are now at the precipice of a paradox – they either maintain current while increasing inference costs to deliver better results or hold inference costs constant and risk dropping out of the race against competitors who invest more computation per query. Because of competitive dynamics pushing towards the former, it puts pressure on already challenging unit economics.If Lockett is right that $10B of OpenAI's revenue was effectively a subsidy from Microsoft, then their operations cost $28B and generated $7B in subscription revenue plus $3B in stuff like licensing. That means that OpenAI was charging subscribers around 25% of what they were costing. To make ends meet subscription costs would need to be 4 times higher, or $80/month. The number of their users who would feel this worth paying is much less than 40 million.

11 comments:

Will Lockett's OpenAI Is Headed For Bankruptcy focuses on Sam Altman's decision to pollute ChatGPT's answers with ads:

"Back in May of 2024, Altman openly stated that ads would be a “last resort” for OpenAI, which makes the decision damn surprising — except when you pause to think about it for a second.

OpenAI’s pitch was that their AI would be so useful and boost people’s productivity so much that everyone would have to buy it just to keep up. That is what drove its insane hype, investments and valuation. OpenAI embedding adverts completely annihilates that narrative. It proves that their AI isn’t even delivering a few dollars a month worth of value to users, let alone the preposterous promises Altman has been yapping about for years.

...

Google receives more than five trillion searches per year and generates $48.5 billion annually in ad revenue from those searches. Not bad.

Let’s assume that, somehow, ChatGPT fully replaces Google as the default internet query machine, meaning it now receives five trillion queries a year and garners $48.5 billion in annual ad revenue from those searches. Well, currently, each word ChatGPT generates costs them $0.0003, and a ChatGPT search responds with 30 words on average, meaning a single search query costs OpenAI $0.01. So, just processing these five trillion queries alone will cost OpenAI $50 billion, meaning these ads will run, at best, at a marginal loss!"

n this post I quoted Will Lockett's skepticism about OpenAI's clain of $20B annual revenue, but being conservative he and I both used it. In OpenAI Is In A Far Worse Position Than I Thought he admits:

"In a previous article, “OpenAI’s Insane Scaling Problem”, I made a mistake. Much to my accountant father’s shame, I confused Annualised Recurring Revenue with Annual Recurring Revenue. As such, I thought OpenAI had claimed to have made $20 billion in revenue last year.

....

OpenAI’s $20 billion ARR figure originated from a blog by OpenAI CFO, Sarah Friar. She took the revenue OpenAI made in December 2025 and then multiplied it by 12 to ‘annualise’ it. This means she is claiming OpenAI made $1.66 billion in December 2025.

OpenAI had previously stated they made $5.5 billion in annualised revenue in December 2024 and $10 billion in annualised revenue in June 2025. If we assume linear revenue growth between these points (Dec 2024, June 2025, and Dec 2025), we can estimate that OpenAI’s total revenue for 2025 was actually $11.9 billion.

...

Multiple analyses have found that OpenAI’s operating costs will be around $28 billion in 2025 (Zitron & The Information). Based on our more realistic $11.9 billion 2025 revenue estimate, that means OpenAI is likely to incur a net loss exceeding $15.6 billion in 2025.

That is nearly double the predicted loss for 2025 and triple their net loss of 2024!"

Via Matt Levine we find Stephen Foley's Moody’s alert cites gap in data centre accounting for Big Tech companies:

"A gap in US accounting rules allows Big Tech companies to conceal tens of billions of dollars of potential liabilities for their AI data centres, the credit rating agency Moody’s warned on Monday. ...

In some cases, companies are taking relatively short-term leases while at the same time guaranteeing to pay compensation if they do not renew and the value of the data centre falls as a result.

The arrangement means liabilities might not show up anywhere in the accounts, according to Moody’s.

US generally accepted accounting principles require the lease renewal to be “reasonably certain” — typically viewed as 70 per cent likely, at least — before it is accounted for. The cost of the residual value guarantee which might be triggered if the lease is not renewed only has to be accounted for if it is “probable”, meaning more than 50 per cent likely."

Levine notes:

"If there’s a 60% chance that you’ll renew, then there’s only a 40% chance that the residual value guarantee will pay out, so the renewal is not “reasonably certain,” the residual value guarantee is not “probable,” and the liability disappears. Nice work!"

Shira Ovide's This economic idea transfixed Wall Street and Washington. It may be a mirage. makes an important point:

"Technology companies’ massive spending on artificial intelligence accounted for half or more of U.S. growth last year, some economists calculated, effectively propping up an otherwise anemic economy.

...

Prominent economists, including from Morgan Stanley and JPMorgan Chase, calculate that the AI buildup was directly responsible not for 92 percent or 39 percent of gains to the U.S. economy in 2025, but as little as zero.

“It was a very intuitive story,” said Joseph Briggs, who jointly leads global economics investment research at Goldman Sachs. “That maybe prevented or limited the need to actually dig deeper into what was happening.”

Briggs and his Goldman Sachs colleagues recently said that investment spending on AI made “basically zero” difference in U.S. economic growth last year.

...

That’s because the $31 trillion in yearly U.S. gross domestic product, the widest measure of the economy, tallies only the final value of products and services produced domestically. Spending on imports and foreign made components is subtracted because it boosts the economies of other countries, not that of the United States.

...

Roughly three-quarters of the cost of an AI data center is for the computer gear and parts such as computer chips that go inside of it, technology analysts estimate. America’s AI champions, including the computer chip pioneer Nvidia, manufacture many of their products in Asia — despite efforts by the Biden and Trump administrations to reduce U.S. dependence on essential chips made overseas."

Les Barclays does the math on the securitization of the debt used to but Nvidia racks in Collateralized Chip Obligations (CCOs). Along the way he summarizes the argument I made here and in Depreciation:

"As Brian DeChesare notes, the real issue in the AI CapEx debate is not whether Big Tech is using 3‑, 4‑ or 6‑year useful lives for GPUs, but the relationship between depreciation, replacement CapEx and the incremental cash flows those assets actually generate. Accounting choices can shift reported earnings, yet on a cash basis the key question is whether the very high AI CapEx ever produces enough durable revenue to justify constant reinvestment."

The whole post is well worth reading.

In Why Are We Still Doing This?, Ed Zitron tears in to what will happen when the AI platforms actually need to cover their costs instead of burning VC money:

"The obvious argument that you could make is that Anthropic could simply increase the price of the subscription product, but I need to be clear that for any of this to make sense, it would have to do so by at least 300%, and even then that might not do the job. This would immediately price out most consumers — an $80-a-month subscription would immediately price out just about every consumer, and turn this from a “kind of like the cost of Netflix” purchase into something that has to have obvious, defined results. A $400-a-month or $800-a-month subscription would make a Claude or ChatGPT Pro subscription the size of a car payment. For a company with 100 engineers, a subscription to Claude Max 5x would run at around $480,000 a year."

Or:

"Let’s say that Anthropic and OpenAI immediately decide to switch everybody to the API. How would anybody actually budget? Is somebody that pays $200 a month for Claude Max going to be comfortable paying $1000 or $1500 or $2500 a month in costs, and have, at that point, really no firm understanding of the cost of a particular action?

First, there’s no way to anticipate how many tokens a prompt will actually burn, which makes any kind of budgeting a non-starter. It’s like going to the supermarket and committing to buy a gallon of milk, not knowing if it’ll cost you $5 or $50.

But also, suppose a prompt doesn’t quite return the result you need, and thus, you’re forced to run it again — perhaps with slightly altered phrasing, or with more exposition to ensure the model has every detail you need. And again, you have no idea how many tokens the model will burn. How does a person budget for that kind of thing?"

Ed Zitron also points out another way AI companies are fudging their accounts:

"Training is, for an AI lab like OpenAI and Anthropic, as common (and necessary) a cost as those associated with creating outputs (inference), yet it’s kept entirely out of gross margins. To quote The Information: “Anthropic has previously projected gross margins above 70% by 2027, and OpenAI has projected gross margins of at least 70% by 2029, which would put them closer to the gross margins of publicly traded software and cloud firms. But both AI developers also spend a tremendous amount on renting servers to develop new models—training costs, which don’t factor into gross margins—making it more difficult to turn a net profit than it is for traditional software firms.

This is inherently deceptive [on the part of Anthropic]. While one would argue that R&D is not considered in gross margins, training isn’t gross margins — yet gross margins generally include the raw materials necessary to build something, and training is absolutely part of the raw costs of running an AI model. Direct labor and parts are considered part of the calculation of gross margin, and spending on training — both the data and the process of training itself — are absolutely meaningful, and to leave them out is an act of deception."

The answer, if there is an answer, is that it won't come from regular users, the same way that Amazon's operating profit doesn't come from consumers (but from AWS).

Ed Zitron is back with another jeremiad, The AI Industry Is Lying To You:

"Hundreds of gigawatts of data centers in development equate to 5GW of actual data centers in construction.

Hundreds of billions of dollars of GPU sales are mostly sitting waiting for somewhere to go.

Anthropic’s constant flow of “annualized” revenues ended up equating to literally $5 billion in revenue in four years, on $25 billion or more in salaries and compute.

Despite all of those data centers supposedly being built, nobody appears to be making a profit on renting out AI compute.

AI’s supposed ability to “write all code” really means that every major software company is filling their codebases with slop while massively increasing their operating expenses. Software engineers aren’t being replaced — they’re being laid off because the software that’s meant to replace them is too expensive, while in practice not replacing anybody at all."

Just go read the whole thing.

Michael Thomas reports that The World's Largest Planned Data Center Is Running Into Trouble:

"Last October, Fermi America raised $746 million in an IPO to build what it claimed would be the largest data center in the world. The company successfully pitched investors on a massive campus it tentatively called the President Donald J. Trump Advanced Energy and Intelligence Campus. (The company now generally refers to it as Project Matador.)

Speed and scale were key to Fermi’s pitch. The company told investors it expected to make $1.5 billion in revenue for every 1 GW of capacity built. It said it expected to launch the first one million square feet of space by April 2026 and generate 1 GW of power by the end of 2026. Fermi originally pitched an 11 GW campus; it later increased the targeted capacity to 17 GW.

On its website, the company says that the “initial phase of construction [is] already complete.” But the company has still yet to begin constructing its first buildings, according to Cleanview’s satellite tracker."

I've been writing for nearly a year that the AI companies were running drug-dealer's algorithm, "the first one's free", because they had an almost unlimited supply of VC money. Once the customer was addicted, and the VC money ran low, they would have to raise prices and enshittify the product to get into profit. Now, David Gerard's Claude Code rate limits: Anthropic AI squeezes the customers documents them doing it, because:

"Anthropic touts “annual recurring revenue” of $14 billion to $20 billion a year. That’s a very fudged number for marketing how cool they are. Anthropic’s actual revenue — that they’re willing to state in legal filing — is a bit over $5 billion in the company’s entire history up to March 9th, 2026:

Although the company has generated substantial revenue since entering the commercial market — exceeding $5 billion to date …

And Anthropic’s spent at least $10 billion on training and inference. So it’s time to cut costs!"

Ed Zitron puts numbers to the extent of the subsidy in Four Horsemen of the AIpocalypse:

"Anthropic’s growth story is a sham built on selling subscriptions that let users burn anywhere from $8 to $13.50 for every dollar of subscription revenue and providing a brittle, inconsistent service, made possible only through a near-infinite stream of venture capital money and infrastructure providers footing the bill for data center construction.

...

If Anthropic were forced to charge its actual costs — and no, I don’t believe its API is profitable no matter how many people misread Dario Amodei’s interview — its growth would quickly fall apart as customers faced the real costs of AI (which I’ll get to in a bit). If Anthropic was forced to provide a stable service, it would have to stop accepting new customers or massively increase its inference costs."

Post a Comment