|

| Source |

|

| Source |

There is certainly a strong argument that the extraordinary boom in tech stocks over the past decade was largely fueled by the unprecedented low-interest-rate policies in response to the global financial crisis of 2008. With capital becoming a commodity, it made sense for opportunistic companies such as Uber to grab as much cash as VC firms would give them to “blitzscale” their way to market domination.Below the fold, I look at how this is now all unwinding.

This madcap expansion was accelerated by funding provided by a new class of non-traditional, or tourist, investors, including Masayoshi Son’s SoftBank and “crossover” hedge funds such as Tiger Global.

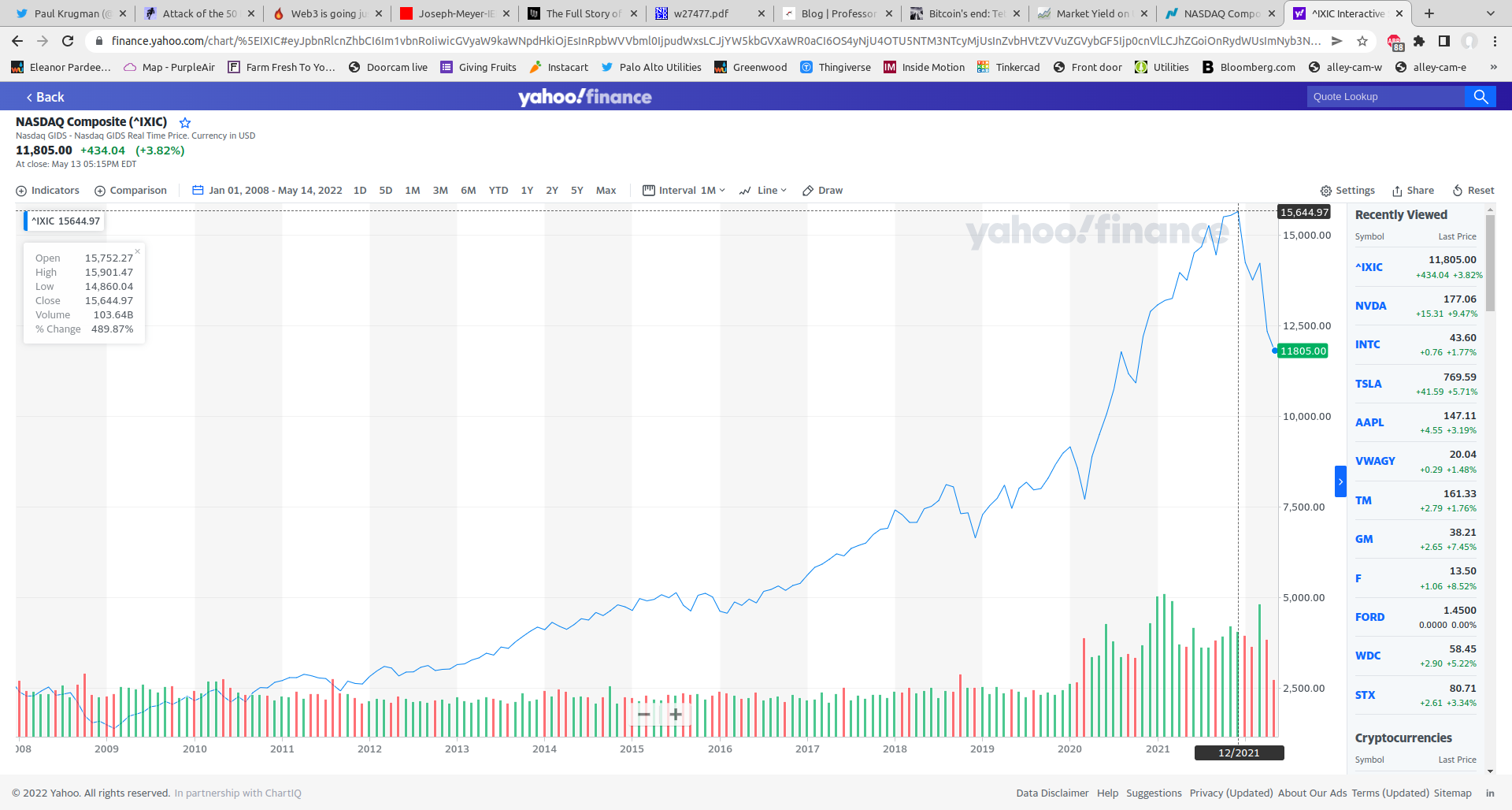

Notionally, the price of a stock reflects the Net Present Value of the company's future flow of earnings. The lower the expected interest rate and the higher the expected earnings, the higher the price. Price-earnings (PE) ratios for leading technology stocks reached levels that imply rapid earnings growth for decades into the future. Once it became clear that interest rates were going up significantly, these PE ratios became unsustainable, and the stock prices dropped as shown in the graph of the NASDAQ index. Given that real interest rates are not yet significantly above zero, they likely have further to fall. To take just one example, Nvidia's PE is still in the mid-40s.

This is a particular problem for VCs. There is no point in them putting money into a company if they can't later get many times the amount out. The price at which they can sell a company, especially one of the newly fashionable kind that hasn't ever actually made a profit, goes down as interest rates go up. Thornhill writes:

Life is already becoming uncomfortable for late-stage startups looking to exit. The public markets are now hard to access. According to EY, the value of all global IPOs in the first quarter of 2022 dropped 51 percent year on year. The once-manic market for special purpose acquisition companies, which enabled highly speculative tech companies to list through the backdoor, has all but frozen. Trade sales have also fallen as M&A activity has contracted sharply. And valuations for late-stage funding rounds have now dropped in the US, with the rest of the world following behind.The VCs have been pouring part of this cornucopia of funds into cryptocurrency and Web3 companies. I discussed the reason why VCs prefer this space to more conventional companies in List And Dump Schemes, based on Fais Khan's "You Don't Own Web3": A Coinbase Curse and How VCs Sell Crypto to Retail. Khan writes:

In spite of this, the VC industry remains stuffed with cash and desperate to invest. According to KPMG, almost 1,400 VC funds around the world raised a total of $207 billion last year.

If coins, especially VC-backed coins, consistently underperformed Bitcoin/Ethereum after listing on Coinbase, that says to me that insiders were waiting for a big, dollar-based exchange to list so they could sell - VCs taking profits at the expense of retail. Those insiders include venture capital firms like a16z and, incredibly, Coinbase’s own venture arm, which has a number of investments listed on Coinbase. Other exchanges like Kraken, FTX, and Gemini are also all active in venture, and have listed their own investments.Khan shows that, after an initial pop, the longer a VC-backed coin has been on Coinbase, the worse it performs relative to BTC and ETH, and:

A16z’s returns are much worse than Coinbase’s listings overall! This to me smells of insider selling. These should be the best coins there are, given a16z’s access, but instead 100% of those older than 12 months and 90% older than 6 months lag Ethereum.The attraction of listing and dumping for VCs is that they can get their money out quickly. In The Unstoppable Grift: How Coinbase and Binance Helped Turned Web3 into Venture3, Khan writes:

They’re collectively shoveling what will probably amount to $10B this year into the crypto startup market - enough for 300 $30m Series A’s. Honestly, I had to laugh writing that. Like a poor French goose, whatever half-decent startups might be out there in crypto land are probably being hounded by hungry investors, while the market gets drowned in a flood of new coins.Nicholas Weaver describes the process:

With hundreds of millions in liquidity available less than one year from investment, that creates a snowball effect. Trading revenues turn into VC rounds that turn into more trading revenues. How else has a16z gone from a $300M fund to $2.5B to $4.5B in less than four years? If these VCs are serious about the “web3” ethos of full transparency, they should be doing far more to disclose their holdings.

Brian Armstrong says Coinbase wants to be the Amazon of assets, which I guess would make him the Jeff Bezos. But to me these exchanges are more like Travis Kalanick at Uber - racing ahead of regulators, hoping to make enough money to pay whatever fines will inevitably come their way.

Frankly, I wouldn’t call investing and then exiting low quality projects within a year by selling to retail “VC” at all - it’s GC, Grift Capitalism, with insiders and exchanges as judge and jury. And I doubt anything will stop it until someone is in handcuffs.

But how they work now is basically securities fraud by inducement. So they invest in a cryptocurrency-related company. They strongly encourage that cryptocurrency company to issue a token that acts as a promise for some eventual service, like say dental care or an orange tree in Florida. And they sell that token to the venture capitalists at a huge discount. So the venture capitalists get a huge pile of these tokens. And then what happens is they encourage the company to go out and sell the token to the general public. And ideally they get that token listed on CoinBase, which is partly owned by Andreessen Horowitz. And if not, they just use the decentralized exchanges or whatever.

And now the venture capitalist is able to sell their tokens to retail investors. This is blatantly an unlicensed security. This is blatant securities fraud, but they didn’t commit the securities fraud. It was just the companies they invested in that did the securities fraud, and the SEC has not been proactively enforcing this. They only retroactively enforce against the initial coin offerings after they fail. So what will happen is Andreessen Horowitz and company invested in a bunch of startups that all issued tokens, that all got dumped on retail including Andreessen Horowitz dumping a lot of them on retail, and when things fail, the only people to prosecute are the companies, not Andreessen Horowitz itself. So they’ve been able to make securities fraud a business in such a way that they are legally remote, so you will not be able to throw them in jail.

|

| Source |

The VCs and the exchanges have vast marketing budgets to induce FOMO in retail investors to support their dumps, including celebrity shilling and Super Bowl advertisements.

When these twoTruly an honor to introduce and welcome former President @BillClinton and former Prime Minister Tony Blair to @CryptoBahamas to cap off an incredible Day 3. pic.twitter.com/3aYMpQtYOr

— Anthony Scaramucci (@Scaramucci) April 28, 2022

|

| Source |

Thirteen days after the Clinton/Blair hype-fest it briefly hit $28K, $40K down from the peak, and it has stayed under about $30K ever since. Why this failure to proceed moonwards?

You will notice I've been quoting the Bitcoin "price" in US dollars (USD). This is convenient but wrong. Very little of the trading in Bitcoin and other cryptocurrencies is in USD, because most exchanges on which the trades are done cannot access the US banking system. The dominant exchange for both spot and derivative trades is Binance, which is so sketchy that it claims not to be headquartered anywhere so not to be under any country's jurisdiction.

Early in the cryptocurrency era this lack of a way to store "dry powder" away from the volatility of cryptocurrencies such as Bitcoin, waiting for the next buying opportunity or for a way out to buy the Lamborghini, led to the creation of Tether (USDT) and other "stablecoins". The initial claim was that each USDT represented a USD in a bank account, so the value of a USDT was "pegged" to $1. It pretty soon became clear that the claim wasn't true, but by then the whole house of cards had become so dependent on the belief that USDT = USD that speculators ignored the lack of backing and just carried on trading as if the backing existed. In practice, arbitrageurs found profit in deviations of stablecoins from their peg, causing them to go away.

This was despite the facts that Tether admitted in court that they had lied about the backing, that they consistently failed to produce an audit, and that multiple articles pointed out Tether's apparent market manipulation. They responded to drops in Bitcoin's price by flooding the market with USDT that could only be used to buy cryptocurrencies and thus drive Bitcoin's price up.

Recently, stablecoins have been in demand as a place to store the results of the selling that has pushed cyrptocurrency prices down.

|

| Tether's Risks |

Levine makes an important point, that this is a system with two relatively stable states, state A when Luna has non-zero value, and state B when it has zero value. So this actually isn't an "algorithmic stablecoin", it is actually an "algorithmic metastablecoin". Wikipedia explains:

- You wake up one morning and invent two crypto tokens.

- One of them is the stablecoin, which I will call “Terra,” for reasons that will become apparent.

- The other one is not the stablecoin. I will call it “Luna.”

- To be clear, they are both just things you made up, just numbers on a ledger. (Probably the ledger is maintained on a decentralized blockchain, though in theory you could do this on your computer in Excel.)

- You try to find people to buy them.

- Luna will trade at some price determined by supply and demand. If you make it up on your computer and keep the list in Excel and smirk when you tell people about this, that price will be zero, and none of this will work.

- But if you do a good job of marketing Luna, that price will not be zero. If the price is not zero then you’re in business.

- You promise that people can always exchange one Terra for $1 worth of Luna. If Luna trades at $0.10, then one Terra will get you 10 Luna. If Luna trades at $20, then one Terra will get you 0.05 Luna. Doesn’t matter. The price of Luna is arbitrary, but one Terra always gets you $1 worth of Luna. (And vice versa: People can always exchange $1 worth of Luna for one Terra.)

- You set up an automated smart contract — the “algorithm” in “algorithmic stablecoin” — to let people exchange their Terras for Lunas and Lunas for Terras.

- Terra should trade at $1. If it trades above $1, people — arbitrageurs — can buy $1 worth of Luna for $1 and exchange them for one Terra worth more than a dollar, for an instant profit. If it trades below $1, people can buy one Terra for less than a dollar and exchange it for $1 worth of Luna, for an instant profit. These arbitrage trades push the price of Terra back to $1 if it ever goes higher or lower.

- The price of Luna will fluctuate. Over time, as trust in this ecosystem grows, it will probably mostly go up. But that is not essential to the stablecoin concept. As long as Luna robustly has a non-zero value, you can exchange one Terra for some quantity of Luna that is worth $1, which means Terra should be worth $1, which means that its value should be stable.

metastability denotes an intermediate energetic state within a dynamical system other than the system's state of least energy. A ball resting in a hollow on a slope is a simple example of metastability. If the ball is only slightly pushed, it will settle back into its hollow, but a stronger push may start the ball rolling down the slope.

By Georg Wiora

{kind=link}

|

| Source |

The token of this long-abandoned project never achieved its target of dollar parity, sank below $1 in early 2021 and was trading well below 1 cent on Wednesday.Shortly after this $54.5M demonstration of the risks of algorithmic metastablecoins Do Kwon, a cryptocurrency whale, launched another algorithmic metastablecoin called Terra (UST) using a companion coin Luna (LUNA) that had been launched earlier. It is now alleged that "Rick Sanchez" and Do Kwon are the same person and an insider is quoted as describing "Basis Cash" as "a pilot program".[2]

|

| Source |

|

| Source |

Instead of just owning Terra (and hoping the peg holds) or not owning Terra, you have the option of betting against it, trying to profit from the peg breaking. It seems to be more or less accepted wisdom that the loss of Terra’s dollar peg was caused by an attack, by someone intentionally selling UST in order to make money from the loss of the peg. (One popular, somewhat complicated form of this theory is that someone got long UST and short Bitcoin, then dumped their UST and made money from the falling price of Bitcoin as LFG sold it to defend the UST peg.)

|

| Source |

Despite the "iron will of unstoppable code", Molly White reported that Terra blockchain is halted after token crash increases threat of governance attacks:

After $LUNA dropped below $0.01, Terra announced that they halted the Terra blockchain. "Terra validators have decided to halt the Terra chain to prevent governance attacks following severe $LUNA inflation and a significantly reduced cost of attack", they wrote on Twitter. This means that no transactions can continue on the Terra chain, and that holders of any tokens based on that chain (including the TerraUSD stablecoin or LUNA) can't do anything with those tokens.Because the cryptocurrency ecosystem is tightly connected, stopping the blockchain had repercussions. Other platforms depended upon "oracles" reporting the "prices" of coins, including UST and LUNA, which were no longer available. White's Unexpected oracle data in the wake of Terra blockchain halt enables multiple attacks on other platforms explained:

Terra only announced this after halting the network, giving their users no opportunity to try to withdraw funds. They have made no announcement about whether or when they intend to bring the network back online, although it seems safe to assume that the enormous loss of confidence in Terra would make any restart short-lived.

Earlier today, Terra halted their blockchain after a devastating few days. Subsequently, Chainlink's oracle paused the price feed, causing it to fall out of sync with the apparent market price of the token. This enabled multiple attacks on various platforms.Jonathan Greig has more details in Collapse of Luna cryptocurrency leads to $11 million exploit on Venus Protocol. Tether briefly lost its peg, spending "six hours below $0.99—at one point slipping down to $0.95—in the most significant deviation from its peg in recent history". Another algorithmic metastablecoin, DEI lost its peg too:

$13.5 million was fraudulently borrowed from the Venus protocol on BSC. Blizz Finance on Avalanche reported their protocol had been entirely drained, amounting to around $8.3 million. Blizz subsequently announced in a post-mortem that "Blizz has no treasury or development fund and a significant portion of the stolen assets belonged to our team. As such we regret to announce the protocol has been paused and we do not intend to resume operations."

DEI, an algorithmic stablecoin created by Deus Finance on the Fantom network, de-pegged on May 15. Intended to be pegged to the US dollar, the token dipped to a low of around $0.50, and continued to hover well below its intended price through the next day. DEI had a nominal market cap of more than $88 million before losing its peg.One lesson

This is another bump in the road for Deus Finance, which lost a total of $16.4 million in two separate flash loan attacks in March and April 2022.

When times were good — when Terra was popular and Luna was valuable — the LFG printed a bunch of valuable Luna and used them to buy a lot of Bitcoins. And so this week the LFG had a lot of Bitcoins, and could use them to buy Terra in the market. (Or, equivalently and more intuitively, sell the Bitcoins for dollars and use the dollars to buy Terra.)This may not have been what actually happened to the stash of Bitcoin. Did Terra operators bail out crypto whales? by Paul Amery reports:

The operators of the collapsed Terra stablecoin ($UST) last week allowed selected holders of the dollar token to cash out at close to 100 cents in the dollar, using cryptocurrency exchanges Gemini and Binance as a conduit.Might it be possible that the "holders of $2.7bn in face value of $UST" included insiders? Who can tell.

According to the Luna Foundation Guard, which operates a reserve pool backing $UST and its related token, $LUNA, holders of $2.7bn in face value of $UST were able to sell them for bitcoin in two transactions last week, one with an effective bitcoin/UST exchange rate of $32,334 and the other with an effective exchange rate of $35,054.

...

It did not disclose the timing of the transactions. However, evidence from Elliptic, a cryptocurrency research firm, suggested that the transactions took place on May 9 and early on May 10, when the $UST price traded in secondary markets as low as 60 cents in the dollar.

...

The two exchanges are now likely to come under increasing pressure to disclose which cryptocurrency market participants were able to exit their Terra stablecoin positions last Monday and Tuesday at close to par value, while retail holders of Terra and Luna have lost nearly all their money.

Not to worry. After losing first $54.5M then $41B, Olga Kharif and Muyao Shen report that Do Kwon Proposes Creating Another Blockchain From Terra’s Ashes:

Kwon wants to copy the blockchain’s code to create a new network, called Terra, and to distribute new tokens to former Terra supporters like key app developers, those whose computers order transactions on the network, and those who still hold TerraUSD, Kwon wrote in a post on a research forum.What could possibly go wrong?

This is a long post but I have barely scratched the surface of the available material on this fascinating week. Here is a "further reading" list:

- David Gerard's The Cryptocurrency Crash Is Replaying 2008 as Absurdly as Possible

- Izabella Kaminska's:

- Robert Burnson's Coinbase Customers Sue Over Stablecoin That Was ‘Anything But’

- Robert McCauley's How stablecoins are destabilising crypto

- JP Konig's A quick note on Tether redemptions during the current crypto bloodbath

- Bryce Elder's Runtime error: stablecoin not found

- Robin Wigglesworth's Synthetic reverse FUD

- Philip Lagerkranser's Crypto’s $270 Billion Meltdown Gives Way to an Uneasy Calm

- Matt Ott and Ken Swee's Bitcoin Tumbles In Wild Week For Cryptocurrency

- David Liedtka's:

- Hannah Miller's Terra $45 Billion Face Plant Creates Crowd of Crypto Losers

- Joe Weisenthal and Tracy Alloway's Meet the Hedge-Fund Manager Who Warned of Terra’s $60 Billion Implosion

- Rebecca Ackermann's Crypto is weathering a bitter storm. Some still hold on for dear life

- David Gerard points out that there was at least one attempt at an "algorithhmic stablecoin" before Ethereum launched in July 2015. In 2014 Bitshares peg lasted 5 days, as documented by Preston Byrne before and after the event.

-

There are a number of inconsistencies in Sam Kessler and Danny Nelson's article:

- The price history of the LUNA half of the UST/LUNA pair starts 7/29/2019 on conmarketcap.com, a long time before the price history of UST starts on 11/24/2020.

- The price history of BAC on conmarketcap.com starts 12/1/2020, which is a week after the launch of UST. So how could it have been a "pilot program" for UST?

- The technology underlying UST uses two coins, whereas that underlying BAC uses three:

Basis Shares and Basis Bonds are used to help keep Basis Cash at a price of $1. If the price falls below this level, bonds can be purchased at discount prices — and redeemed on a 1:1 basis once prices exceed this level.

If BAC remains above $1 after bonds have been redeemed, new BAC tokens are minted and distributed to those who own Basis Shares. - According to coinmarketcap.com, BAC went well above $1 and didn't lose the peg until 1/6/2021.

- If Do Kwon was behind both UST and BAC, why did he want two metastablecoins?

10 comments:

In How a Trash-Talking Crypto Founder Caused a $40 Billion Crash, David Yaffe-Bellany and Erin Griffith note that:

"The downfall of Luna and TerraUSD offers a case study in crypto hype and who is left holding the bag when it all comes crashing down. Mr. Kwon’s rise was enabled by respected financiers who were willing to back highly speculative financial products. Some of those investors sold their Luna and TerraUSD coins early, reaping substantial profits, while retail traders now grapple with devastating losses.

Pantera Capital, a hedge fund that invested in Mr. Kwon’s efforts, made a profit of about 100 times its initial investment, after selling roughly 80 percent of its holdings of Luna over the last year, said Paul Veradittakit, an investor at the firm.

Pantera turned $1.7 million into around $170 million."

Where did that $168.3M come from? Retail traders. It is all about ripping off the muppets.

Molly White has two headlines in quick succession that could possibly be related:

1) Terraform Labs' legal team resigns.

2) Class action lawsuits filed against Terra founders after crypto collapse.

Bryce Elder's Barclays to tether: the test is yet to come discusses a report from Barclays pointing out that Tether and similar cryptocurrencies claiming to be fully backed are also metastable, albeit their arbitrage barriers are higher than those of algorithmic metastablecoins. The report asserts:

"The only way to get immediate access to fiat is to sell the token on an exchange, regardless of the size of holding . . . [W]hile redemption is ‘guaranteed’ at par, the secondary market price of tether can trade lower, depending on the willingness of holders to accept a haircut in return for access to immediate liquidity. As last week’s price action suggests, some investors were willing to accept a nearly 5 per cent discount to liquidate their USDT holdings immediately.

We think that willingness to absorb losses, even though USDT is fully collateralized and has an overnight liquidity buffer that exceeds most prime funds, suggests the token might be prone pre-emptive runs. Holders with immediate liquidity demands have an incentive (or first-mover advantage) to rush to sell in the secondary market before the supply of tokens from other liquidity-seekers picks up. The fear that USDT might not be able to maintain the peg may drive runs regardless of its actual capacity to support redemptions based on the liquidity of its collateral."

In other words, the combination of the restrictions on USDT wthdrawals, and the chain of counterparty risk behind it, limit the height of its arbitrage barrier.

Not a moment too soon. Emily Nicolle's Terra Collapse Triggers $83 Billion Decentralized Finance Slump reports:

"The collapse of one of decentralized finance’s most ambitious experiments has knocked more than $83 billion off the sector’s total value, as investors fled for safer havens.

A crash in the prices of stablecoin TerraUSD, or UST, and its sister token Luna in the first half of May sent shock waves through the DeFi sector, where investors borrow, lend and stake cryptocurrencies without intermediaries like banks. The total value locked across all major protocols has slumped to $112 billion from $195 billion at the start of the month, data from industry tracker DeFi Llama show."

Scott Chipolina and George Steer's The Terra/Luna hall of shame is a salutary list of the promionent shills whose faces are now covered with egg.

Jialiang David Pan's Ethereum Founder Buterin Blasts DeFi Model in Terra Critique starts:

"Ethereum founder Vitalik Buterin said there is no genuine investment that can get anywhere close to 20% returns per year while analyzing the implosion of the Terra blockchain which sent the crypto market into freefall earlier this month."

But he is still having difficulty coming to terms with reality:

"The high-profile developer also explores viable mechanisms to maintain automated pure-crypto stablecoins’ pegs while appealing not to dismiss the entire category. He defines automated stablecoins by characteristics such as a completely decentralized targeting mechanism that tracks a price index, and unlike Tether and USDC does not rely on any asset custodians.

Buterin also suggests more rigorously evaluating how safe systems are by looking at their steady state, as well as their pessimistic state to see how they perform under extreme conditions and whether they can safely wind down. He also warns of other risks associated with automated stablecoins such as technical glitches."

This seems like a list that would make you agree with Prof. Hilary Allen.

See Buterin's Two thought experiments to evaluate automated stablecoins.

More good news for Terra from Molly White:

1) Researcher discovers vulnerability in the Terra Mirror Protocol that allowed attackers to siphon tens of millions from the project:

"A crypto researcher who goes by "FatMan" discovered that the Mirror Protocol in the Terra ecosystem contained a serious vulnerability, that was quietly patched with no announcement on May 9. The Mirror Protocol code previously lacked a duplicate check, which meant that attackers could create a short position and then withdraw it repeatedly in the same transaction, taking many times more money than they should have been authorized to withdraw.

FatMan discovered one instance where a person deposited $10,000 and later withdrew $4.3 million. According to FatMan, they found repeated exploits of this type that earned attackers "well over $30 million". Another researcher on Terra forums estimated about $88 million had been exfiltrated from the project in this way, over the many months the bug went undiscovered and unpatched by Mirror developers."

2) Luna 2.0 airdrop sends 2.1 million $LUNA to Mirror Protocol thief:

"All holders of Luna, who saw their holdings crash to nothing in the Terra collapse, received an airdrop of the new Luna tokens with the release of Terra 2.0 (electric boogaloo). The researcher who originally observed that at least $88 million worth of ill-gotten tokens had been siphoned from the Terra Mirror Protocol before a patch was quietly applied in early May noticed that the attacker had been among the recipients of the airdrop, receiving more than 2.1 million $LUNA."

Matt Levine has an interesting analysis of how the collapse of UST/LUNA differs from a normal bankruptcy in Terra Is Back From Bankruptcy.

"In traditional finance terms, Terra went bankrupt, and reorganized, and its shareholders got more of a recovery than its creditors. Not how things work in traditional bankruptcy!

...

Nobody is going around buying algorithmic stablecoins because they are confident that they’ll get paid back first if the ecosystem blows up. (They are buying them for … uh … other reasons? Confusion? Faith in the algorithm? Intense desire for this to work?) So, when the ecosystem blows up, there is no reason to pay the stablecoin holders first."

And:

"In broad outlines, some holders of UST got paid roughly $1 for their UST out of the LFG money, and some did not and held through the collapse. If you are a suspicious person, you might ask questions like “wait, were certain favored insiders cashed out at $1 while other retail bagholders got nothing?” But if you are a traditional finance person, you might ask simpler questions like “why should anyone have been cashed out at $1 when there clearly wasn’t enough money to go around?”"

In 2021's BUILT TO FAIL: THE INHERENT FRAGILITY OF ALGORITHMIC STABLECOINS Ryan Clements describes a whole other set of reasons why algorithmic stablecoins are actually metastable:

"First, they require a support level of demand for operational stability. Second, they rely on independent actors with market incentives to perform price-stabilizing arbitrage. Finally, they require reliable price information at all times. None of these factors are certain, and all of them have proven to be historically tenuous in the context of financial crises or periods of extreme volatility."

Emily Nicolle's Mystery of Terra Collapse Deepens With Possible FTX Role Raised has a pretty detailed account of the actions behind the Terra/Luna collapse that illustrates how the selling pressure overrode the arbitrage defending the UST peg and drove it over the metastability barrier. The Feds are investigating the role Alameda played in generating the sell pressure:

"Kaiko also found that funding rates and volumes suggested that someone was aggressively shorting Luna. But because the LFG was so focused on spending Bitcoin to help shore up UST on Anchor and Curve, there was relatively little left to match the massive sell wall that its price was facing on exchanges.

The bulk of those “sell” orders against UST appeared to be coming from Alameda, the person cited by the New York Times said. US officials declined to comment when reached by Bloomberg News."

FTX Founder Sam Bankman-Fried Is Said to Face Market Manipulation Inquiry by Emily Flitter, David Yaffe-Bellany and Matthew Goldstein broke the story of the investigation:

"Federal prosecutors are investigating whether FTX’s founder, Sam Bankman-Fried, manipulated the market for two cryptocurrencies this past spring, leading to their collapse and creating a domino effect that eventually caused the implosion of his own cryptocurrency exchange last month, according to two people with knowledge of the matter.

U.S. prosecutors in Manhattan are examining the possibility that Mr. Bankman-Fried steered the prices of two interlinked currencies, TerraUSD and Luna, to benefit the entities he controlled, including FTX and Alameda Research, a hedge fund he co-founded and owned, the people said."

Post a Comment