Last October I wrote

Non-Fungible Token Bubble Lasted 10 Months. The NFT market is still dead, a fossil relic of a massive wave of typical cryptocurrency pump-and-dump schemes and wash trading. But the great thing is that this all happened on a public blockchain, so data palaeontologists have an unrivalled dataset with which to unearth the inner workings of a speculative bubble.

Bryce Elder's

What NFT mania can tell us about market bubbles points us to

NFT Bubbles in which Andrea Barbon and Angelo Ranaldo do just that. Their abstract states:

Our study reveals that agent-level variables, such as investor sophistication, heterogeneity, and wash trading, in addition to aggregate variables, such as volatility, price acceleration, and turnover, significantly predict bubble formation and price crashes. We find that sophisticated investors consistently outperform others and exhibit characteristics consistent with superior information and skills, supporting the narrative surrounding asset pricing bubbles.

Below the fold I discuss the details.

Elder explains why this is a particulary revealing dataset:

As well as being absent of any fundamental value, NFTs were practically impossible to short or hedge, so they appealed almost exclusively to retail punters. Add in public blockchains that give each trade provenance and traceability, and we have what’s probably the first diagrammatic description of how the actions of individuals foment a madness of crowds.

|

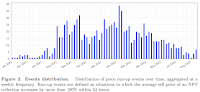

Figure 1

|

During the bubble, NFTs exhibited wild swings in price and volume although a generally decreasing trend as shown in Barbon and Ranaldo's Figure 1. Their research focused on whether it was possible to predict these swings, and whether there were sophisticated market players capable of using these predictions to profit from the ups and avoid the downs.

They write:

The key question that motivates our research is whether the predictive power of asset bubbles is more effectively discerned by scrutinizing the conduct of individual investors. In line with the asset bubble narrative, we posit that if there exists a larger cohort of sophisticated investors with a heightened degree of skill and expertise, their augmented presence should predict fewer incidents of speculative bubble bursts. Three main results stand out from our analysis: First, aggregate variables such as high volatility, price acceleration, and low turnover significantly predict crashes. Second, some investors persistently perform better than others, and their characteristics suggest that they are more sophisticated, with superior information and skills. Third, a greater presence of sophisticated agents in the price run-up significantly decreases the risk of a subsequent crash and increases ex-post positive returns. In contrast, a smaller number of individual investors and more price manipulation through “wash trading” increase the crash risk and predict more illiquidity in the crash phase, thus exacerbating the adverse effects.

|

Figure 2

|

Barbon and Ranaldo's Figure 2 shows that they identified a large number of "run-up events", during which "the average sell price of an NFT collection increases by more than 100% within 24 hours". Thus the "sophisticated players" had a lot of price spikes to exploit. The next question was whether they were able to catch the upside of the spike and avoid the downside:

They write:

we aim to investigate whether certain investors consistently outperform others, that is, whether there exists a group of sophisticated investors who possess the ability to generate gains by riding successive price run-ups while avoiding price corrections. This would serve as a first indication of their sophistication. To this end, we compute the percentage profits obtained by individual investors during the entire run-up event window of [−24, 24]. We find that the profitability of investors is strongly autocorrelated across different run-up events, with a significant autoregressive coefficient of 0.21 (t-stat = 27.59). These results imply that some investors consistently excel at riding price run-ups and avoiding crashes, while others consistently perform poorly.

|

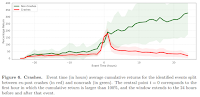

Figure 5

|

The next question was whether these "run-up events" subsequently crashed rather than resulting in a persistent gain.

The authors's Figure 5 shows the distribution of crashes and non-crashes; they

define a crash thus:

we define an event as a crash if the ex-post return realized during the 24 hours following the run-up identification is lower than −40%. According to this criterion, we find that about 52% of the events result in a crash, ex-post. This is not surprising: a high proportion of incidences was expected given the high volatility and fast-paced growth of the NFT market.

|

Figure 6

|

Their Figure 6 shows that the difference in returns between non-crashes and crashes is enormous, greatly rewarding the ability to predict which the spike will be.

Who were these "sophisticated" players able to make such predictions? Barbon and Ranaldo

write:

First, the agent’s profitability is persistent across run-up events, suggesting that some agents possess more advanced abilities to perform consistently better over time. Second, outperforming agents are distinguished in terms of (a) greater market presence, (b) financial leverage, and (c) sharper timing. In addition to trading more volume and frequently, their activity spans multiple exchanges (crossmarket trading), they are more likely to provide liquidity and to trade in decentralized exchanges (DEX), like Uniswap, Balancer, or Curve, and they leverage up their positions to exploit profit opportunities and access arbitrage capital through decentralized lending platforms. Furthermore, these investors are more skilled in timing the bubbles, by both buying early into the run-up phase and selling close to the peak of the bubble. All in all, the more sophisticated behavior of outperforming investors suggests that some individuals possess superior information and skills in identifying NFT investment opportunities, timing the market movements, and avoiding being caught in the bursting of NFT bubbles.

One thing the authors are careful not to suggest is that the reason "these investors are more skilled in timing the bubbles, by both buying early into the run-up phase and selling close to the peak of the bubble" is that "these investors" are

causing the bubbles through their use of social media and the pumping effect of their "buying early". Although they acknowledge the presence of wash trading they play down its significance,

writing:

we analyze wash trading at the aggregate and transaction levels, identifying suspicious trades empirically. Although this practice of price manipulation is not widespread in OpenSea and in our data set, we find that when wash trading is more pervasive ex-ante, ex-post crashes and liquidity deterioration are more likely.

This conflicts with the reports of high-profile wash trading in the NFT market and endemic wash trading in broader cryptocurrency markets, such as those I discussed in

Making Sure "Number Go Up". For example, Nick Baker's

An NFT Just Sold for $532 Million, But Didn’t Really Sell at All dissects a blatant example:

The process started Thursday at 6:13 p.m. New York time, when someone using an Ethereum address beginning with 0xef76 transferred the CryptoPunk to an address starting with 0x8e39.

About an hour and a half later, 0x8e39 sold the NFT to an address starting with 0x9b5a for 124,457 Ether -- equal to $532 million -- all of it borrowed from three sources, primarily Compound.

To pay for the trade, the buyer shipped the Ether tokens to the CryptoPunk’s smart contract, which transferred them to the seller -- normal stuff, a buyer settling up with a seller. But the seller then sent the 124,457 Ether back to the buyer, who repaid the loans.

And then the last step: the avatar was given back to the original address, 0xef76, and offered up for sale again for 250,000 Ether, or more than $1 billion.

And the abstract of

Crypto Wash Trading by Lin William Cong reads:

We introduce systematic tests exploiting robust statistical and behavioral patterns in trading to detect fake transactions on 29 cryptocurrency exchanges. Regulated exchanges feature patterns consistently observed in financial markets and nature; abnormal first-significant-digit distributions, size rounding, and transaction tail distributions on unregulated exchanges reveal rampant manipulations unlikely driven by strategy or exchange heterogeneity. We quantify the wash trading on each unregulated exchange, which averaged over 70% of the reported volume. We further document how these fabricated volumes (trillions of dollars annually) improve exchange ranking, temporarily distort prices, and relate to exchange characteristics (e.g., age and userbase), market conditions, and regulation.

Finally, Joanna Ossinger reports that a

Small Group of Insiders Is Reaping Most of the Gains on NFTs, Study Shows:

a new study from Chainalysis shows that a small portion of participants reap most of the gains.

Investing frequently in a wide array of collections appears to lead to the highest profits, Chainalysis said in its report. It added that whitelisting -- the practice of allowing a certain set of followers or others to purchase new NFTs at a much lower price than other users during minting events where a digital file is turned into a digital asset on a blockchain-- helps those people significantly.

Users who make the whitelist and later sell their newly-minted NFT gain a profit 75.7% of the time, versus just 20.8% for users who do so without being whitelisted,

...

“A very small group of highly sophisticated investors rake in most of the profits from NFT collecting,” the study said. “This is especially true in minting, where the whitelisting process gives early supporters of collection access to lower prices that result in greater profits. We also see possible evidence of the use of bots by investors looking to purchase during minting events, which could shut out less sophisticated users, and even result in failed transactions that cost them in fees.”

4 comments:

I'm shocked, shocked to find that wash trading is going on in here! Erik Larson and Yueqi Yang report that Celsius Investors Claim Crypto Market Maker Aided ‘Wash Trading’:

"Wintermute Trading Ltd., one of the biggest cryptocurrency market makers, was accused in a proposed class-action lawsuit of helping former Celsius Network Ltd. Chief Executive Officer Alex Mashinsky dupe investors in his now-bankrupt crypto lending firm.

Plaintiffs who sued Mashinsky and other Celsius executives in July 2022 amended their federal lawsuit in New Jersey this week to add London-based Wintermute as a defendant, entangling another major industry player in the fallout from Celsius’s collapse.

Wintermute engaged in “wash trading” — which creates the illusion that an asset is trading far more often than it actually is — and other improper activities starting in March 2021 to inflate the value of Celsius’s native CEL token and loan products, according to the suit."

DappGambl's Dead NFTs: The Evolving Landscape of the NFT Market is devastating:

"Of the 73,257 NFT collections we identified, an eye-watering 69,795 of them have a market cap of 0 Ether (ETH).

This statistic effectively means that 95% of people holding NFT collections are currently holding onto worthless investments. Having looked into those figures, we would estimate that 95% to include over 23 million people who’s investments are now worthless.

...

Of the collections we identified, only 21% were fully spoken-for, in terms of having 100%+ ownership. This means that 79% of all NFT collections – otherwise known as almost 4 out of every 5 – have remained unsold.

...

our study identified 195,699 NFT collections with no apparent owners or market share. The energy required to mint these NFTs is comparable to 27,789,258 kWh, resulting in an emission of approximately 16,243 metric tons of CO2.

...

A startling 18% of these top collections have a floor price of zero, indicating that a significant portion of even the most prominent collections are struggling to maintain demand.

Furthermore, 41% of the top NFTs are modestly priced between $5 and $100, which may signal a lack of perceived value among these digital assets.

Astonishingly, less than 1% of these NFTs boast a price tag of over $6,000, shedding light on the rarity of high-value assets even within the cream of the crop."

Tim Copeland's DWF Labs denies report that it did $300 million of wash trading on Binance last year isn't a surprise:

"The Wall Street Journal alleged that when Binance hired a raft of top investigators in 2022, they found evidence of rampant market manipulation on the exchange, citing sources. At the time, these investigators recommended removing several hundred users for violating the terms of use.

In late 2023, this surveillance team claimed that DWF Labs had manipulated the price of the YGG token and at least six other tokens, the WSJ said, and processed more than $300 million of wash trades that year — recommending the client be removed.

Binance launched an investigation into the surveillance team itself and the evidence it had found, and claimed that there was insufficient evidence of such activities. A week later, the exchange fired the head of the surveillance team and then rejected the request to remove the trading firm, the WSJ said."

Ben Weiss' Sunk Costs is a must-read account of the dumpster fire that is OpenSea. But despite losing money, staff, market share and credibility the fire will take a long time to burn out:

"It was losing about $30 million in the first three quarters of 2023, according to an internal document I obtained. (It, however, projected that the November layoffs would reduce the company’s overhead in 2024.) And in June, the trading volume on its platform reached lows not previously seen since before the NFT boom in early 2021, per DappRadar.

OpenSea still has plenty of runway. It had $438 million in cash and $45 million in crypto reserves as of November 2023, according to an internal document, and it’s coasting on that capital as it hopes a “2.0” pivot will help it navigate choppy seas."

Post a Comment