The TL;DR of the series is that, assuming Tether has turned over a new leaf and is being honest about USDT being backed by USD:

- There should be a big pile of USD somewhere.

- The logical place for it to be is in US banks.

- The logical US banks for it to be in are the two US "crypto banks", Silvergate and Signature.

- US banks have to report to regulators.

- These reports show a set of coincidences that suggest this is where the reserves are.

First we are going to go through two US banks that hold a lot of crypto-related USD. Then we are going to look how remarkably their balance sheets resemble the quantity of USDT outstanding. And finally we are going to hint at a fascinating connection between those banks’ purported source of USD and a potential “crypto big hitter” source.

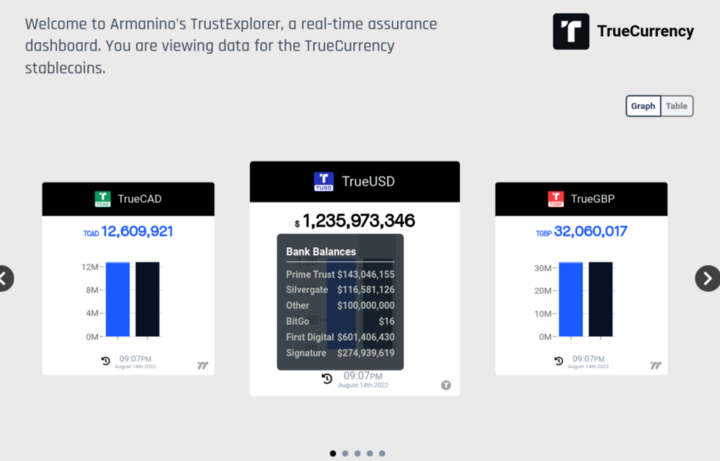

|

| Source |

So there has been a pile of actual USD sitting in two banks that closely matches the issuance of USDT:

This is not Tether’s cash surely. At least not directly. But what is it?Tether used to claim that most of their allegedly one-for-one backing was "commercial paper", which normally consists of a loan a company with excess cash made to a company in need of cash. This isn't like that, but:

First, this proves enough cash looks to have entered the ecosystem to back Tether. Absolutely nobody is claiming these US banks are lying about their deposit liabilities to both the SEC and FDIC.

...

We are not asserting Tether has all of this cash or that they are honest. But it does look like enough cash came in one way or another. There is cash somewhere.

...

Second, it suggests a theory. Maybe Tether’s commercial paper consists of obligations of whoever owns these USD deposits. Again there is money here and if one company promises it to another there is a sense in which that is commercial paper.

It is a horrible abuse of the language but promising someone else your bank deposit is similarly some kind of a certificate of deposit or maybe cash-equivalent/accounts receivable thing.Presumably, having a contract with another company saying "if we need it we can draw on your accounts at Silvergate and Signature" is enough for Tether to issue that amount of USDT. And both sides hope they won't need it. A year ago, in Anyone Seen Tether’s Billions?, Zeke Faux went looking for Tether's "commercial paper":

Elsewhere on the website, there’s a letter from an accounting firm stating that Tether has the reserves to back its coins, along with a pie chart showing that about $30 billion of its dollar holdings are invested in commercial paper—short-term loans to corporations. That would make Tether the seventh-largest holder of such debt, right up there with Charles Schwab and Vanguard Group.The explanation seems to be that what Tether means by "commercial paper" is not the kind of asset the commercial paper market trades.

To fact-check this claim, a few colleagues and I canvassed Wall Street traders to see if any had seen Tether buying anything. No one had. “It’s a small market with a lot of people who know each other,” said Deborah Cunningham, chief investment officer of global money markets at Federated Hermes, an asset management company in Pittsburgh. “If there were a new entrant, it would be usually very obvious.”

Next, Minor Stablecoins & USDT Issuance: Even More Coincidences (August 19th) starts:

Here we analyze the flows into a collection of “minor” stablecoins and find a remarkable connection between these tokens and USDT issuance. And — importantly — we find that this pattern does not hold for USDC and BUSD. Those stablecoins are widely used and do not look like this sort of funnel into USDT.First, HUSD:

...

What do we mean by minor stablecoins? HUSD, TUSD, USDP, GUSD. There is also USDK but it’s so tiny the word “minor” doesn’t do it justice.

GUSD & USDP likely everyone will agree are properly USD backed and perform something like the required KYC/AML checks. The other two…let’s just say questions have been raised.

HUSD is an odd stablecoin. First, it’s not particularly large in market cap terms but sure has a lot of minting and burning

...

they switched over to Stable Universal from Paxos as the stablecoin service provider

Which seems to be an odd outfit in that they still take payments into Silvergate bank:

...

Stable Universal is taking payments into the same accounts that Huobi referenced above. And they are a strange outfit in that, despite all the US banking stuff, they don’t take US customers:

So Huobi and this HUSD are a bit weird. But there is a plausible route for them to have all the USD. And, at least in part, those USD sit at US banks. Huobi Trust is a licensed (in Nevada) financial services business in the US so they should have no trouble moving money into the US banking system.

|

| Source |

Recognize some of those bank names? Good. From here on our we are going to assume these things are all backed by real USD and that, to a large extent, those USD migrate to Silvergate and Signature. There is ample reporting that these folks all bank at the same two places.

|

| Source |

We know these stablecoins interact with the same banks as the USDT-sized pile of dollars we found last time. Now let’s compare USDT market cap against the cumulative burning of these stables:

We can see based on the shape of the combined minor stable, USDC and BUSD burns that the two “more normal looking” stables take off much later and bend more aggressively. All three are on the same secondary axis at the same scale. There is an uncanny correspondence between USDT growth and the amount of funds being burned through these minor stablecoins.

|

| Source |

Here is burning of the minor stables vs issuance of USDT on Ethereum and TRON:So, the story so far is that these minor stablecoins are used as a channel to get USD into Signature and Silvergate, where it is used to back USDT.

Pretty tight connection during 2019-2020 no? These are all on the same axis.

Another coincidence: Huobi announced support for USDT on TRON in March 2019 and Poloniex in April 2019. Those are right after Tether started supporting TRON.

Stablecoin Cyclones: Mint & Burn Patterns (August 29th) starts asking where the USD flowing into the minor stablecoins is coming from:

The point here is that the mechanism we offered last time as pure speculation — that these stablecoins are used as vehicles to get USD into the “major crypto banks” — is not just plausible but consistent with a lot of on-chain data. And this data reveals direct connections among precisely the parties we would expect if that narrative is correct.And explains what the hypothesis would imply:

If these coins were useful we would expect to see most tokens out there floating around various protocols. We would expect lots of inter-exchange transfers and flows within DeFi. But most importantly we would expect to see long routes between mints and burns as the coins are used for real things throughout their lives. Sure, some people will mint and then redeem but that makes no sense as the main use case.They examine all four coins but HUSD is the most interesting:

Now, we already know there is a lot of burning. So the best we can hope for is a range of circuitous routes through the ecosystem as tokens experience real economic uses before finally being redeemed.

What we do not expect to find in a useful coin is a large number of short, high volume routes from mint to burn. What economic purpose does that serve? Think of cash in the real world: how often do you withdraw a lot of money from the bank, pay someone, and they then go deposit that cash back in the bank? And what is really happening there?

First we found nearly a thousand addresses and not a single one of them minted and burned. But both sides look to be proper addresses. We were able to tag the largest minter (0x5f64d9c81f5a30f4b29301401f96138792dc5f58) as Huobi and the 3rd largest minter (0x83a127952d266a6ea306c40ac62a4a70668fe3bd) as Alameda.So what is really going on?

Also some of these wallets — like 0x5586a235b4c5eff57b8b65f77a97780d9347fa47 — look like staging wallets off of exchanges (Huobi in this case). All they do is receive tokens from Etherscan-tagged exchange wallets and then burn them. One imagines somewhere an operations person is checking the tokens arrived, redeeming the real USD, and then burning the tokens. Maybe it’s automated — it doesn’t really matter precisely how it works.

The largest burner (0x4bd0244d26df7780a56df2f20c53b507e35cb373) looks like a staging wallet out of the one we found above tagged Binance (0xE25a329d385f77df5D4eD56265babe2b99A5436). Now recall we already know everyone involved banks at the same handful of places with the suspiciously-USDT-like cash balances.

So what do we see here? We see Huobi, Alameda and Binance minting and redeeming a lot of these things out of different wallets. And it’s not like the wallets just rotate over time — many many wallets are used for years on both sides. These look very much like individual exchange-adjacent client wallets, minting and redeeming out of different sources.

...

These are billions of dollars in tokens that are not used for trading flowing from source, through a pair of exchanges in close proximity, and then back to sink.

This could not look more like an effort to obfuscate capital flows if it tried. Yes it is plausible this is all bog-standard economic activity. But recall, again, what else we know: USD at the “crypto money center” banks tracks USDT well, and USDT-on-TRON tracks these stablecoin burns well.The problem that these minor stablecoins are solving is how to turn fiat currency into balances in Tether, the most widely accepted stablecoin. The fiat buys one of the minor stablecoins at some loosely regulated exchange, and redeems it for USD at one of the "crypto-banks". The USD then "buys" USDT, not by transferring USD to Tether but by increasing the value represented by "commercial paper".

Now we know that the former head of TRON is involved directly in the process. We also know these burns are happening out of places that bank at the major banks — and that freshly minted tokens often make their way there before returning home to the null address.

Does this prove beyond all doubt these are conduits for USD to get redeemed at Signature/Silvergate and then back USDT? No. Does it show how closely the empirical evidence matches a world where that is happening? Yes. Yes it does.

The summary of USDT-on-TRON, FTX & WTF Is Really Happening (September 7th) is:

FTX/Alameda minted nearly all the USDT-on-TRON and operate as something like a central bank or reserve manager for a shadow East Asian USD payment system. We provide convincing evidence from novel on-chain analysis that shows how a real, albeit mostly-not-kosher, crypto use case works. This data also makes plain that Binance/Cumberland runs the Ethereum part of the same ecosystem and that these two groups of parties probably coordinate their actions in some way.Here is the background:

...

we are going to show that this entire complex looks an awful lot like a funnel to establish backing for a USD payment network aimed at people who cannot (easily or legally, depending) hold USD or transfer them. This also exposes how USDT is split into a China-and-surroundings slice and a rest-of-world slice with a different major crypto entity handling each part.

"This video" is a detailed description of the "shadow East Asian USD payment system" by QCP Capital, based in Malaysia. You should definitely watch it. It explains how international trade in this area is denominated in USDT because it is faster, cheaper and less visible to the authorities.

- USDT is used in the real world for all kinds of “grey area” stuff. This video again.

- Crypto is formally illegal in China. Including stablecoins.

- USD are generally inaccessible, or heavily restricted, in China.

- TRON, and Huobi Eco Chain, are big in stablecoin transactions in China and adjacent/similar places.

|

| Source |

|

| Source |

This is all a pretty convincing story, but there are some contradictions. In August Datafinnovation suggested that ~$77B at Signature and Silvergate was backing USDT. But in May Jaimie Crawley reported that Tether Cut Commercial Paper Reserve by 17% in Q1, Accountants Say:

Tether reduced its commercial paper holdings by 17% from $24.2 billion to $20.1 billion in the first quarter, according to its latest attestation report.At the same time Tether's Paolo Ardoino tweeted:

The majority of this $20.1 billion (around $18 billion) is comprised of A-1 and A-2 paper, which qualify as investment grade, according to the report. A list of ratings agencies grading the commercial paper wasn't specified other than, "Standard & Poor’s ratings, or equivalent ratings by Moody’s, Fitch or other nationally recognized statistical rating organizations" in the footnotes. The geographic location of the commercial paper issuers was also not found in the report.

The reduction in commercial paper has continued with a further 20% cut since April 1, which will be reflected in the second-quarter report, Tether announced Thursday. On June 30, 2021, commercial paper and certificates of deposit totaled $30.8 billion, or 49% of Tether's assets at that time.

Tether has also slightly reduced its cash deposits from $4.2 billion to $4.1 billion and increased its U.S. Treasury bond holdings from $34.5 billion to $39.2 billion since its last report.

The "other investments" category, which includes digital tokens, has remained consistent, falling slightly from $5.02 billion to $4.96 billion.

If Tether had been buying government bonds there should have been an outflow of USD from their reserves, but this doesn't show up in the reports from the crypto banks. So maybe the pile of USD that Datafinnovation found in these banks isn't Tether's reserves and the coincidences that they found are really coincidences. If so, that leaves two questions. First, where are Tether's reserves? And second, whose is the big pile of USD in the crypto banks? It is related to "digital assets", but which?#tether Q1 2022 attestation is out.

— Paolo Ardoino 🍐 (@paoloardoino) May 19, 2022

17+% reduction of commercial papers in Q1 2022. Also Q2 looking great, current reduction of CP over Q1 is already 20+%. Moved all to US treasuries. Portfolio avg maturity has gone down a lot, improving liquidity at hand. Thanks all. https://t.co/VXo6JPQy36

This all supports the need for regulation of cryptocurrencies in general but, in particular stablecoins. Paige Smith's Fed’s Barr Says Stablecoins Are Urgent Risk Requiring Guardrails starts:

A top Federal Reserve official warned Congress that it needed to pass legislation with strong crypto guardrails to prevent future financial-stability risks.

Entities offering stablecoins -- cryptocurrencies pegged to a separate asset -- are an urgent risk that must be addressed, because they’re backed by the dollar and “really borrow the trust of the Federal Reserve,” Fed Vice Chair for Supervision Michael Barr said Wednesday before the US House Financial Services Committee.

It’s “important for Congress to step in and say you’re not permitted to offer a stablecoin unless it’s done under a strong prudential framework with Federal Reserve oversight, supervision, regulation and approval,” Barr said. “Private money can create enormous financial-stability risks, unless it’s appropriately regulated.”

Throughout the committee hearing, Barr reiterated that it’s Congress’s role to intervene. He said bills should include a strong role for Fed oversight of stablecoins, which he called a form of private money.

4 comments:

Dirty Bubble Media's One of these stablecoins is not like the others... assesses the backing for USDC, BUSD and USDT:

"Of these stablecoins, the Tether stablecoin is the largest with a current market capitalization of $65 billion, followed by Circle ($43 billion) and BUSD ($22 billion). By daily trading volume, Tether also (usually) dominates the market. Other than a brief period during the FTX failure when BUSD volume skyrocketed (???), Tether’s volume typically outpaces the other two stablecoins by several fold ... In other words, Tether serves as the primary source of dollar liquidity in cryptocurrency markets."

As regards USDC:

"Despite the caveat that these statements are unaudited, Circle’s disclosure provides a fairly good level of detail about the assets backing their reserves. They hold a relatively simple mix of liquid and low-risk assets that would be easy to liquidate in case holders of their stablecoin wanted to redeem their dollars."

As regards BUSD:

"the BUSD reports provide substantial detail about the reserves backing the stablecoin. And, like USDC, the composition of the stablecoin’s reserves is simple and composed entirely of low-risk assets."

But Amy Castor and David Gerard note:

"BUSD is a Paxos-administered dollar stablecoin. Each BUSD is backed by an alleged actual dollar in Silvergate Bank, and attested by auditors. (If not actually audited as such).

That’s true of BUSD on the Ethereum blockchain. It’s not true of BUSD on Binance.

BUSD on Binance is on their internal BNB (formerly BSC) blockchain, bridged from Ethereum. It’s a stablecoin of a stablecoin. Binance makes a point of noting that Binance-BUSD is not subject to the legal controls that Paxos BUSD is under."

As regards USDT:

"Tether’s disclosures and reserves strategy differs wildly from its major competitors. Their attestations don’t show anywhere near the same level of detail as either Circle or Paxos. Their strategy is far more complex and Tether admits to holding more risky assets on the balance sheet. And, it appears that at least some of Tether’s reserves are held in highly illiquid venture capital investments that may be worth significantly less than what Tether claims they are.

...

Despite issuing loans to other crypto firms, Tether has somehow avoided losses on every single blowup over the past year, from 3AC to Celsius to FTX. This, despite the fact that Alameda Research was the largest recipent of USDT."

Matt Levine explains how Tether pumps the BTC "price":

"here is a story you could tell:

1) You have 1,000 Bitcoin worth about $17 million.

2) You want to buy more Bitcoin, but you do not have any dollars.

3) You go to Tether and say “hey give me 17 million USDT, in exchange I’ll put up 2,000 Bitcoins as collateral.”

4) Tether is like “sure that’s the business we’re in” and hands you 17 million USDT.

5) You use that 17 million USDT — notionally worth $17 million — to buy 1,000 more Bitcoin.

6) Now you have 2,000 Bitcoin.

7) You post the 2,000 Bitcoin as collateral to Tether for the loan, which is now overcollateralized with liquid collateral ($34 million worth of Bitcoin).

8) More USDT have been created to buy Bitcoin, but no new dollars have come into the system."

Matt Levine discusses the difficulties of shorting USDT:

"So in round numbers the way to make a $100 million bet against Tether is (1) you take $100 million of your own money, (2) you park it with some crypto counterparty to borrow 100 million Tethers, (3) you sell those Tethers, (4) Tether goes to zero, (5) you buy back the Tethers for $0, (6) you go back to your counterparty and say “here’s my 100 million Tethers, can I have my $100 million back,” and (7) your counterparty is just a smoking crater and your $100 million is gone. Being short Tether is a lot like being long Tether."

Yves Smith reports that Crypto-Focused Silvergate Bank Got De Facto Backdoor FDIC Bailout via $4.3 Billion Federal Home Loan Bank Advance:

"because Silvergate focused on handling fiat-currency transactions of crypto traders…like FTX, Alameda Research, Gemini, and Coinbase. when it was hit by a bank run, it went to the Federal Home Loan Bank system for a $4.3 billion bailout. Silvergate could do that because in its old boring days as a traditional bank, it was in the mortgage business and hence had access to the Federal Home Loan Bank facilities, and maintained them despite its transformation into an institution with a very different risk profile.

...

This incident may explain the sudden issuance at the start of the year of a strictly-worded joint letter by the three national banking regulators, the Fed, the FDIC, and the Office of the Controller of the Currency. They warned that dalliance with crypto and being a bank didn’t fit well together very well."

Post a Comment