Elder's analogy starts by assuming you have £10.

A fairground sells ride tokens for £1.20 each or ten for £10. Some people buy tokens individually. They’re idiots. Others buy ten tokens at a time. They’re also idiots.Your balance sheet now looks like this:

Smart people borrow ten tokens from the ticket booth using £10 as security. The fair value of ten tokens is £12 so it’s a no-brainer.

- Assets: 10 tokens (fair market value £12) + cash £10.

- Liabilities: Debt to ticket booth 10 tokens (fair market value £10).

But instead of going on the waltzers or whatever, they pledge the tokens back to the ticket booth as security for a £10 loan. They now have a £10 loan that’s secured by tokens valued at £12, and a loan of £10 that secures the tokens, which creates £2 of delicious equity.Your balance sheet now looks like this:

- Assets: 10 tokens (fair market value £12) + cash £20.

- Liabilities: Debt to ticket booth 10 tokens (fair market value £10) + £10.

The next smart thing to do is to borrow more tokens from the ticket booth using the money borrowed from the ticket booth that can be loaned back to the ticket booth.Your balance sheet now looks like this:

- Assets: 20 tokens (fair market value £24) + cash £20.

- Liabilities: Debt to ticket booth 20 tokens (fair market value £20) + £10.

Bingo: more equity created. The process can be repeated infinitely because £10 of tickets is always worth £12 and, importantly, there’s no actual fairground. It’s just a ticket booth.Is this magic? No, the equity is being created because of an accounting trick. Here's what your balance sheet should look like after the first step:

- Assets: 10 tokens (fair market value £12) + cash £10.

- Liabilities: Debt to ticket booth 10 tokens (historic cost £10).

|

| Source |

{kind=link}

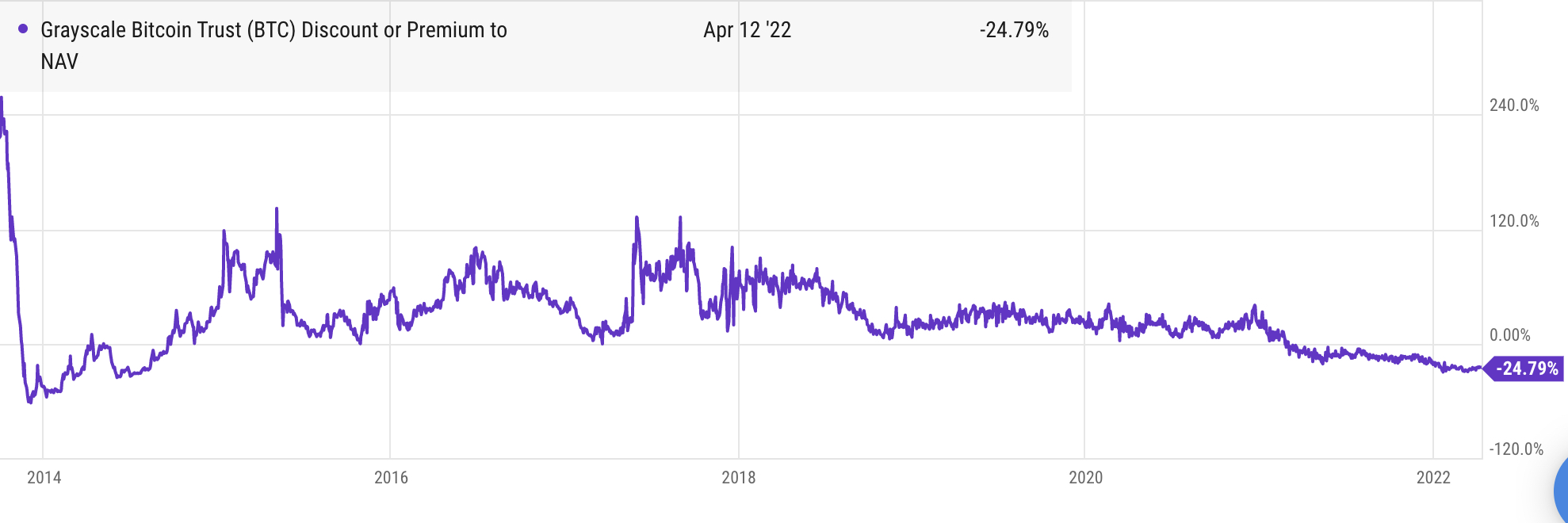

To prevent this infinite money pump spinning out of control, the first twist was that the shares were locked up for 6 months. In effect, buying shares with Bitcoin was a bet that the premium six months ahead would represent interest on the Bitcoin used for the purchase. The second twist was that, as Castor's headline suggested, that the Bitcoin checked in to the trust but they never checked out. The bet was that the premium plus the spot Bitcoin price you got after 6 months would represent replacing your Bitcoin from the market plus the premium as interest. Thus it didn't matter wether Bitcoin went up or down in that time, what determined the interest was the premium at the 6-month mark.

The shares traded at a premium for six years straight, so this was a sure-fire win. And who better to know this than Grayscale Bitcoin Trust itself? So this is where Datafinnovation's investigation comes in:

DCG [Digital Currency Group] owns Grayscale and Genesis. Grayscale issues/manages/etc the GBTC fund which they are desperately trying to turn into an ETF. And Genesis provides borrowing and lending services, among other things, on BTC and GBTC and USD.What is the Digital Currency Group? Dan Primack reports in SecondMarket founder launches bitcoin conglomerate:

GBTC is a US-registered security. Genesis is a US-registered broker-dealer. This means two key things:

- We are talking about securities here, with 100% certainty.

- Both companies file lots of documents with the SEC

It’s called Digital Currency Group, and will include a pair of businesses that were originally formed at SecondMarket, but were not part of the sale to Nasdaq. They include Genesis Global Trading, an over-the-counter bitcoin trading firm; and Grayscale Investments, a digital currency asset management firm that manages the Bitcoin Investment Trust, a publicly-listed vehicle that raised over $60 million.Alas:

Grayscale used to be called SecondMarket. And back when it had that name it had some SEC problemsGiven they were under a cease-and-desist order, Grayscale and Genesis couldn't risk using the money pump themselves. If they were going to benefit from it, they needed (1) a third party to run the pump, and (2) a way for the third party to kick back some of the ill-gotten gains.

...

That is a cease and desist order. Genesis really shouldn’t be messing around with:

activities that could influence artificially the market for the offered security

What Datafinnovation suggests might have happened, based on the timings of a sequence of sales, is that the third party was Three Arrows Capital (3AC):

So what happened here? Well, the guess is the following sequence of events was repeated over and over:Does this sound like Elder's analogy?

Sounds circular right? It is.

- 3AC borrows BTC from Genesis as a lender with some small amount of collateral

- 3AC passes this BTC to Genesis as a Authorized Participant to create GBTC shares. Genesis duly locks the BTC in the trust via Grayscale and returns shares.

- These shares are trading at a premium so this represents “free money” to 3AC.

- 3AC then pledges these shares back to Genesis for a USD loan. If the premium was large enough this loan is worth more than the BTC they borrowed at the beginning.

The money pump worked as long as the shares 6 months ahead traded at a premium, which they did until early 2021. Amy Castor wrote:

Everybody was happy until February 2021, when the Purpose bitcoin ETF launched in Canada. Unlike GBTC, which trades over-the-counter, Purpose trades on the Toronto Stock Exchange, close to NAV. At 1%, its management fees are half that of GBTC. Within a month of trading, Purpose quickly absorbed more than $1 billion worth of assets.So GBTC has 3.4% of all the Bitcoin (maybe 10% of the Bitcoin free float) locked up forever. And because there is no longer any premium, no-one is earning interest on the Bitcoin they used to buy GBTC shares.

Demand for GBTC dropped off and its premium evaporated. Currently, 653,919 bitcoins (worth a face value of $26 billion) are stuck in an illiquid vehicle.

But, just as the spot Bitcoin market is dwarfed by the derivatives market, that's not the real problem. Amy Castor again:

Crypto lender BlockFi’s reliance on the GBTC arbitrage is well known as the source of their high bitcoin interest offering. Customers loan BlockFi their bitcoin, and BlockFi invests it into Grayscale’s trust. By the end of October 2020, a filing with the SEC revealed BlockFi had a 5% stake in all GBTC shares.So the pain was widespread. But worse was to come, as Datafinnovation explains:

Here’s the problem: Now that GBTC prices are below the price of bitcoin, BlockFi won’t have enough cash to buy back the bitcoins that customers lent to them. BlockFi already had to pay a $100 million fine for allegedly selling unregistered securities in 2021.

As of September 2021, 47 mutual funds and SMAs held GBTC, according to Morning Star. Cathie Wood’s ArkInvest is one of the largest holders of GBTC. Along with Morgan Stanley, which held more than 13 million shares at the end of 2021.

If the price is too low there are two big problems:

When the premium started to move DCG stepped in and started buying. Notice the premium disappeared in early 2021 and their buying program began in March 2021.

- 3AC can’t repay the USD loan

- 3AC can’t repay the BTC loan

|

| Source |

3AC sold about half their position to DCG. And pledged the rest for loans to Genesis and Equities First. Because BTC rallied so spectacularly their position was worth over $1 billion and the loans were huge.Why did BTC rally so spectacularly? Amy Castor explains that the huge GBTC premium drove demand for GBTC which drove demand for BTC:

There were several versions of the arb. You could borrow money through a prime broker. You could use futures to hedge your bet. You could recycle your capital twice a year.After 3AC sold to DGC and took out loans, they had a lot of USD. What did Su Zhu and Kyle Davies do with a lot of USD?:

Every version involved Grayscale purchasing more bitcoin, thus increasing demand, widening the spread in the premium, and pushing the price of bitcoin ever higher. Between January 2020 and February 19, 2021, the price of BTC climbed from $7,000 to $56,000.

They spent this money on stuff. We don’t need to go into precisely what but it involved a yacht, houses, LUNA tokens and all manner of shitcoins and other investments.But then:

Now while these two were living monastic lifestyles waiting for a yacht thatBecause they had been running the money pump, 3AC had been able to offer ridiculously high returns, which allowed other firms to offer slightly less ridiculous returns simply by funneling investor money to 3AC. Amy Castor describes the result:

was bought over a year ago and commissioned to be built and to be used in Europe

the prices of stuff they owned collapsed. Why and how LUNA fell apart doesn’t matter here. What matters is that it collapsed. Over the weekend of May 7–8 BTC, and the rest of the crypto market, dropped sharply. GBTC fell back to levels it hadn’t seen since mid 2020.

At this point their GBTC-backed loans were margin-called. They had no more cash and the company fell apart.

Crypto hedge fund Three Arrows Capital (3AC) went into liquidation as it was heavily invested in UST and luna. Firms that had big loans to 3AC, such as Voyager, Celsius, and BlockFi, had to file bankruptcy or seek bailouts from other crypto firms. Even crypto exchanges had been playing the CeFi markets with customer funds, and many had to close their doors.Frances Coppola's Where has all the money gone? provides a lot of detail about 3AC's collapse. The TL;DR is:

And after Luna blew a massive hole in its balance sheet, it robbed Peter to pay Paul, lied to its customers and ghosted the creditors on whose loans it was defaulting.Finally, Datafinnovation points the finger of suspicion:

...

The overall picture that emerges from this, together with the extraordinary series of loan agreements in the bundles, is of a company that was massively over-leveraged and had for some time been experiencing cash flow strain. It borrowed heavily to ride the wave of crypto appreciation during the pandemic. "The money will never run out" was its philosophy. But when the market turned and crypto prices started to fall, it had to borrow even more to maintain its collateral and meet its obligations.

...

But if the company's remaining assets and those of its co-founders have gone to safe havens beyond the reach of liquidators, and the co-founders have fled to a country with no extradition treaties, then creditors will receive little or nothing and legal action will be toothless. And since the failure of companies like Voyager and Celsius was at least partly caused by 3AC's collapse, it is their retail customers who will ultimately pay for Su Zhu and Kyle Davies's recklessness and extravagance.

If this is right then Genesis financed this fiasco. They lent 3AC BTC. And then, effectively, lent them more USD against those very BTC. That sounds absurd. And it is.

No comments:

Post a Comment