Grayscale wants to convert its Grayscale Bitcoin Trust (GBTC) into a bitcoin ETF after flooding the market with shares. GBTC is trading 25% below its net asset value, and investors are rightfully pissed off. Grayscale wants them to be upset with the SEC, but the regulator isn’t really to blame. If anything, the SEC should have warned the public about GBTC years ago.Below the fold, I provide some commentary:

The "Hotel California" reference is to the fact that BTC check in to the trust, whenever someone buys shares either for cash or for BTC, but once they have checked in only 2%/year can ever check out:

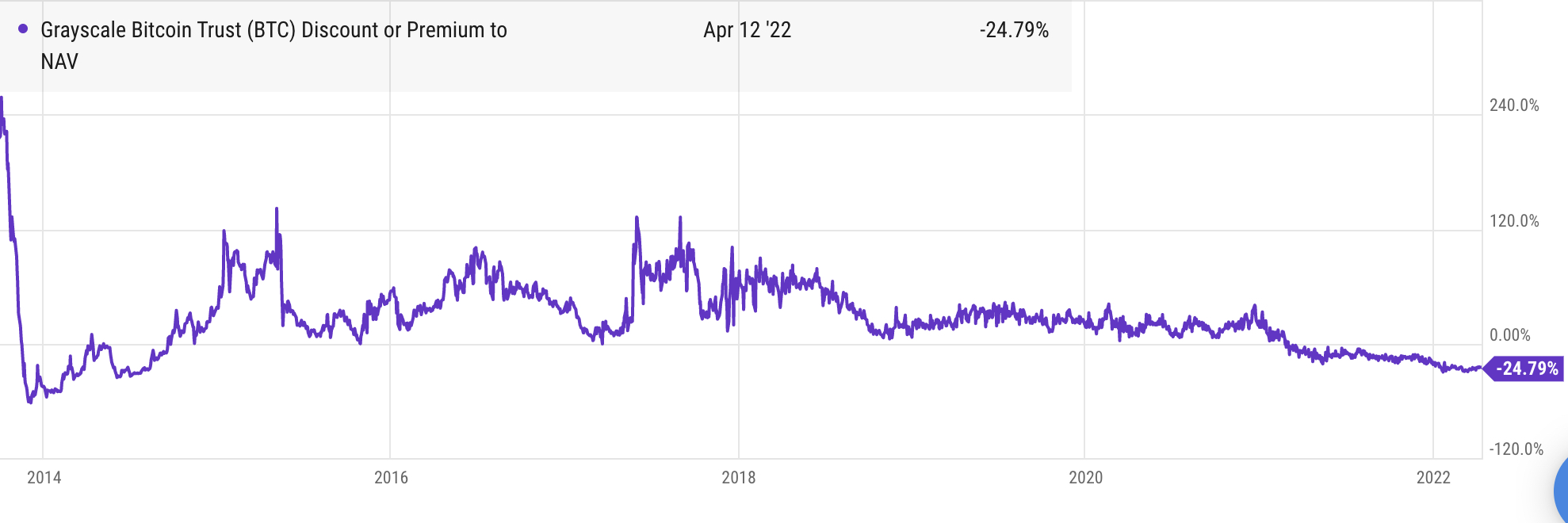

Legally, GBTC is a grantor trust, meaning it functions like a closed-end fund. Unlike a typical ETF, there is no mechanism to redeem the underlying asset. The SEC specifically stopped Grayscale from doing this in 2016. Grayscale can create new shares, but it can’t destroy shares to adjust for demand. Grayscale only takes bitcoin out to pay its whopping 2% annual fees, which currently amount to $200 million per year.The fact that there is a large fund that buys but essentially never sells BTC has an effect on the "price". But in November 2020's Why This Reflexive Ponzi Scheme Will Continue… Harris Kupperman explained that the effect was much bigger than simply demand (my emphasis):

In contrast, an ETF trades like a stock on a national securities exchange, like NYSE Arca or Nasdaq. An ETF has a built-in creation and redemption mechanism that allows the shares to trade at NAV via arbitrage. Authorized participants (essentially, broker-dealers, like banks and trading firms) issue new shares when the EFT trades at a premium and redeem shares when they trade at a discount, making a profit on the spread.

What is GBTC? It is a vehicle that issues new shares daily in exchange for cash or Bitcoins. The shares are issued at the Net Asset Value (NAV), but with the unique wrinkle that they cannot be sold for 6 months. GBTC does not sell Bitcoin except to pay management fees and there is no mechanism in place for it to ever sell Bitcoin like a typical ETF. Think of GBTC as Pac-Man. The coins go in, but do not go out.As everyone

GBTC currently trades at a 26% premium to NAV and has traded at a 18.7% average premium for the past year.This spread provided for a number of ludicrously profitable trades, such as:

You buy GBTC in the daily offering and short free-trading GBTC. Six months later, it all nets out and you are left with your profits. ... You can recycle your capital twice a year and on an unlevered basis, even after paying borrow fees, you’re making north of 40% a yearOr:

sell your GBTC at today’s price and buy it back at NAV through the daily offering (which gets you long about 26% more shares for a bit of paperwork).All of which involve the trust buying ever-increasing amounts of BTC, pumping the "price" ever higher, attracting ever more speculators to these trades, and driving the premium over NAV ever higher. This is why Kupperman calls this a "Reflexive Ponzi Scheme".

Like other Ponizi schemes, this all worked great until it didn't:

Everybody was happy until February 2021, when the Purpose bitcoin ETF launched in Canada. Unlike GBTC, which trades over-the-counter, Purpose trades on the Toronto Stock Exchange, close to NAV. At 1%, its management fees are half that of GBTC. Within a month of trading, Purpose quickly absorbed more than $1 billion worth of assets.

Demand for GBTC dropped off and its premium evaporated. Currently, 653,919 bitcoins (worth a face value of $26 billion) are stuck in an illiquid vehicle. Welcome to Grayscale’s Hotel California.

|

| Source |

{kind=link}

Fed by stimulus money, tethers, and a new grift in the form of NFTs, the price of bitcoin reached a record of nearly $69,000 in November 2021. Bitcoiners rah-rahed the moment.It is easy to see why the holders of GBTC would want to convert it to an ETF that would trade close to NAV. It would give them an instant 33% boost to their current valuation. But Grayscale is in a win-win situation. No matter how unhappy the shareholders are, every year Grayscale gets their 2% fee, "currently worth around $200M", for doing nothing.

However, the same network effects that brought BTC to its heights are working in reverse and can just as easily bring it back down again. At its current price of $40,000, amidst 8.5% inflation, bitcoin is not proving itself to be the inflation hedge Grayscale hyped it up to be.

Among the unhappy shareholders are some pretty sleazy operators. For example:

Crypto lender BlockFi’s reliance on the GBTC arbitrage is well known as the source of their high bitcoin interest offering. Customers loan BlockFi their bitcoin, and BlockFi invests it into Grayscale’s trust. By the end of October 2020, a filing with the SEC revealed BlockFi had a 5% stake in all GBTC shares.Customers loaned BTC to BlockFi, so BlockFi has to give them BTC back. But it can't get the BTC it used to buy GBTC back, they're in the Hotel California. So BlockFi needs to sell the GBTC in the market to get cash to buy the BTC to give back to their customers:

Here’s the problem: Now that GBTC prices are below the price of bitcoin, BlockFi won’t have enough cash to buy back the bitcoins that customers lent to them. BlockFi already had to pay a $100 million fine for allegedly selling unregistered securities in 2021.In a similar vein, Sam Bankman-Fried, the CEO of the FTX exchange, in a Bloomberg interview explained DeFi's "yield farming". Molly White summarizes:

Bankman-Fried launched into an explanation in which he compared it to a box that "they probably dress up to look like [it's] life-changing" but it "does literally nothing". He explained how people put money into the box "because of, you know, the bullishness of people’s usage of the box". "So they go and pour another $300 million in the box and you get a psych and then it goes to infinity. And then everyone makes money."Castor concludes:

[Matt] Levine responded, "I think of myself as like a fairly cynical person. And that was so much more cynical than how I would’ve described farming. You’re just like, well, I’m in the Ponzi business and it’s pretty good."

I encourage anyone reading this to submit your comment to the SEC regarding Grayscale’s application for a spot bitcoin ETF. Jorge Stolfi, a computer scientist in Brazil, has provided an excellent example of how to do this. Quality over quantity is key. Use your own words, tell your own story. Submit your comments here.Here is my comment:

Please DO NOT authorize the Grayscale bitcoin ETF. The reasons why you rejected previous ETF proposals are still valid and should be sufficient to deny this one (and any future ones) as well.

The constant pressure to approve a spot Bitcoin ETF exists because Bitcoin is a negative-sum game - Bitcoin whales need to increase the flow of dollars in so as to have dollars to withdraw. The SEC should not pander to them.

My recent talk to Stanford's EE380 course started by pointing out that cryptocurrencies' externalities include:

Bitcoin is notorious for consuming as much electricity as the Netherlands, but there are around 10,000 other cryptocurrencies, most using similar infrastructure and thus also in aggregate consuming unsustainable amounts of electricity. Bitcoin alone generates as much e-waste as the Netherlands, cryptocurrencies suffer an epidemic of pump-and-dump schemes and wash trading, they enable a $5.2B/year ransomware industry, they have disrupted supply chains for GPUs, hard disks, SSDs and other chips, they have made it impossible for web services to offer free tiers, and they are responsible for a massive crime wave including fraud, theft, tax evasion, funding of rogue states such as North Korea, drug smuggling, and even as documented by Jameson Lopp's list of physical attacks, armed robbery, kidnapping, torture and murder.I went on to discuss in detail the potential for mitigating these externalities and concluded:

Although the techniques used to implement decentralization are effective in theory, at scale emergent economic effects render them ineffective. Despite this, decentralization is fundamental to the cryptocurrency ideology, making mitigation of its externalities effectively impossible. And attempts to mitigate the externalities of pseudonymous cryptocurrencies are lijkely to be self-defeating. We can conclude that:Gateways between cryptocurrencies and the real economy should be illegal, as they impose massive externalities on the real economy. The US is far behind China in realizing this.

- Permissioned blockchains do not need a cryptocurrency to defend against Sybil attacks, and thus do not have significant externalities.

- Permissionless blockchains require a cryptocurrency, and thus necessarily impose all the externalities I have described except the carbon footprint.

- If successful, permissionless blockchains using Proof-of-Work, or any other way to waste a real resource as a Sybil defense, have unacceptable carbon footprints.

- Whatever Sybil defense they use, economics forces successful permissionless blockchains to centralize; there is no justification for wasting resources in a doomed attempt at decentralization.

21 comments:

Mark Gongloff writes Crypto-Backed Mortgages Are as Crazy as They Sound:

"If you entered a contest to see who could design a financial instrument to lose the most money the fastest, you would struggle to come up with a better idea than taking home mortgages backed by crypto, slicing them into mortgage-backed securities and selling them at the moment the global financial system is being bludgeoned by pandemic, war and Jerome Powell.

And yet here we are: Bloomberg News reports the hot new thing in finance is the nouveau crypto riche putting up their expensive digital assets as collateral to buy expensive houses using a more-or-less traditional mortgage, but with no dead-tree dollars down. The brainchild of a company called Milo Credit — based in America’s Crypto Capital, Miami — this offering goes a little further than what we’ve seen so far, which has included the use of crypto for home down-payments and apartment deposits and the occasional crib selling as an NFT."

Note that this reinforces the idea that there aren't enough actual dollars going in to satisfy the demand for actual dollars to come out of the cryptocurrency ecosystem.

The administration probably cannot effectively regulate cryptocurrencies. The likely scenario is that Grayscale Bitcoin Trust sues the SEC for refusing to allow a spot Bitcoin ETF, and Elon Musk seizes the opportunity to neuter the SEC by funding the case and launching a massive Twitter campaign to get it to the Supreme Court, where the Republican justices rule that the SEC's regulatory function is unconstitutional. Decades of Democratic fecklessness have delivered the future Tony Kushner saw in Angels in America, where the Republican courts control the government.

Farhad Manjoo has woken up to the blockchain gaslighting. In What Is Happening to the People Falling for Crypto and NFTs he writes:

"Honestly, I have long tried to keep an open mind to these claims, because I have been incredibly dismayed by the way a handful of firms have taken over an internet that I once thought of as a font of innovation. If there really is a new web that’s going to solve all the problems of the old web, sign me up.

But the continual blowups should crater those expectations. At the same time that the Ethereum blockchain was getting crushed by last weekend’s Bored Apes sale, another supposedly smart crypto network, Solana, was taken offline by bots — one of several full or partial outages it has experienced this year. Two other crypto ventures, Rari Capital and Saddle, were hit with attacks that led to a loss of a combined $90 million in Ether. Early last week, Deus Finance lost $13.4 million in the second attack in two months. I could go on — and on, and on.

There’s also little of the decentralization that we’re being promised. Many web3 companies are funded by the same people who built the web we’re now trying to reform.

Musk didn't have to neuter the SEC, the 5th Circuit did it for him already. @mjs_DC explains:

"The 5th Circuit just dismantled the SEC's power to enforce securities law. This decision is beyond radical. It is nihilistic.

...

Anyway, the implication of this decision is that most (all?) agency enforcement power is unconstitutional. Which, in plain English, means that the federal government can't enforce a huge swath of regulations. I mean, this is basically striking down the administrative state."

More evidence of the dismal prospects for effective cryptocurrency regulation. Rob Pyers tweeted:

"Ah. The Democrats' House Majority SuperPAC, which took some heat for spending $1 million in the #OR06 primary backing Carrick Flynn (who got $11M in support from Sam Bankman-Fried's Protect Our Future PAC), also got $6M from SBF in April."

Hat tip to David Nir at Daily Kos.

Daniel Strauss has a lot more detail on the dismal prospects in The Crypto Kings Are Making Big Political Donations. What Could Go Wrong?:

"An analysis of donations by crypto billionaires (specifically the ones listed on the Forbes 2021 list of the wealthiest Americans) shows that they have donated to a range of Democratic and Republican congressional candidates across the country, as well as state parties and national allied groups.

...

What sets these donors and their support apart from the hordes of other wealthy contributors looking to sway campaigns or just distinguish themselves as political players is that the cryptocurrency field is comparably uncharted ground. Within the Democratic Party, there’s an emerging debate over how much regulation of the cryptocurrency industry there needs to be."

The CFTC sued the Gemini exchange and their press release demonstrates why regulators are so far behind the curve:

"The complaint alleges that from approximately July 2017 to around December 2017, Gemini, directly and through others, made false or misleading statements of material facts, or omitted to state material facts, to the CFTC during an evaluation of the potential self-certification of a bitcoin futures contract by a designated contract market (DCM)."

That is, the CFTC is taking action 54 weeks after the conduct stopped. In December 2017, Bitcoin was near the peak of its first big run-up at around $15K. A lot has happened since.

Sam Sutton's Crypto lobbying hits fever pitch as Bitcoin's favorite senator finishes bill reinforces the dismal prospects for regulation:

"The most highly anticipated legislation in the history of cryptocurrency is about to make its debut, after months of hype drummed up by Sens. Cynthia Lummis and Kirsten Gillibrand.

Lummis, the first-term Wyoming Republican who’s enthralled the Bitcoin faithful with appearances at crypto festivals across the country, has been teasing the contents of her comprehensive digital currency regulation plan in a series of podcast appearances, industry gatherings and high-profile media appearances for much of the past year. Gillibrand, a New York Democrat, hopped on the hype train as a co-author in March, giving the effort a new sheen of bipartisanship."

Allyson Versprille's breathless headline Sweeping US Crypto Legislation Targets Stablecoins, Mining misrepresents a bill that does nothing effective except hand Sam Bankman-Fried what he has been pouring money into lobbying for. Molly White has a more realistic take in Senators Lummis and Gillibrand work across the aisle to please cryptocurrency industry with their proposed legislation:

"A press release from Lummis included statements of support from Kraken, Coinbase, FTX, crypto lobbyists, and various other major players in the cryptocurrency industry—unsurprising support for a bill that is incredibly friendly to the sector. Notably, the bill broadly avoids classifying cryptocurrencies as securities, which would be regulated by the SEC and provide some consumer protections. Instead, the Senators create a foggy definition for sufficiently "decentralized" cryptocurrencies that would treat them as commodities and place them under the purview of the CFTC—the much smaller and less aggressive regulator that has been the preference of most in the cryptocurrency industry."

A new wolf in town?

Pump-and-dump manipulation in cryptocurrency markets by Anirudh Dhawan and Tālis J. Putniņš is yet another study of market manipulation. Their abstract reads:

"We investigate the puzzle of widespread participation in cryptocurrency pump-and-dump manipulation schemes. Unlike stock market manipulators, cryptocurrency manipulators openly declare their intentions to pump specific coins, rather than trying to deceive investors. Puzzlingly, people join in despite negative expected returns. In a simple framework, we demonstrate how overconfidence and gambling preferences can explain participation in these schemes. Analyzing a sample of 355 cases in six months, we find strong empirical support for both mechanisms. Pumps generate extreme price distortions of 65% on average, abnormal trading volumes in the millions of dollars, and large wealth transfers between participants."

Amid the current failure to proceed moonwards (BTC @ $23K, ETH @ $1.2K) we have the regular "money is down for maintenance" phenomenon:

1) Molly White writes in Binance pauses Bitcoin withdrawals for 3 hours due to "stuck" transactions:

"The pause occurred as Bitcoin was reaching record low prices not seen since 2020, contributing to the ongoing pattern of Binance suddenly pausing withdrawals or undergoing maintenance during periods of chaos in the crypto ecosystem."

2) She writes in Celsius pauses all withdrawals, claims it's due to "extreme market conditions":

"There has been a lot of concern lately about Celsius' reserves and its ability to honor redemptions, with some speculating that the platform might be underwater and forced to default.

...

Celsius' June 12 announcement did not include any details on what their plans would be, just that they hoped it would allow them to "stabilize liquidity and operations while we take steps to preserve and protect assets"."

Celsius is an exceptionally sketchy business, whose CFO was arrested last November, and was closely associated with Israeli crypto mogul Moshe Hogeg, also arrested at the same time. They act as a bank offering ludicrous interest rates on cryptocurrency deposits (17%!). Tether made a $62.8M investment in Celsius, and have been lending them USDT in large amounts.

Amy Castor and David Gerard list the current good news for Bitcoin and the rest of the cryptocurrency ecosystem in The Latecomer’s Guide to Crypto Crashing — a quick map of where we are and what’s ahead.

The SEC has rejected the application from Grayscale Bitcoin Trust to launch a Bitcoin ETF. My comment is noted in footnote 72 on page 21. The next step is the Grayscale will sue the SEC. My concern is that the stacked Supreme Court will use this case to neuter the SEC's regulatory authority, as they are about to do to the EPA.

Jonathan Reiter posted an amazing piece of detective work, 3AC, DCG & Amazing Coincidences. The story is complex but the TL;DR is:

"It looks like DCG and 3AC were engaged in some kind of scheme to extract value from the GBTC premium. This provided massive leverage for 3AC which they encashed and used to fund a wide range of things. It also generated a lot of short-term profits for DCG via fees. But 3AC was wildly leveraged and they appear to have gone insolvent over the Terra-Luna weekend. The epic losses from this blowup are only starting to be felt."

David Pan's Grayscale Sets Up Entity to Invest in Bitcoin Mining Hardware reveals yet another scheme to mine a path to prosperity:

"Grayscale Investments, the largest crypto asset manager, is shifting strategy during the midst of the market downturn by setting up an entity seeking to buy Bitcoin mining equipment at distressed prices.

The New York-based firm will form Grayscale Digital Infrastructure Opportunities LLC (GDIO), ... GDIO plans to purchase the computer rigs used in mining and hopes to profit by selling the Bitcoin earned in the process, ... This is likely a three-to-five-year investment"

3-5 years is wildly optimistic. Mining rigs have an economic life of 18-24 months, and these rigs will have already burnt some of that. Pan writes:

"Grayscale is the latest firm aiming to capitalize on the distressed crypto-mining industry. Low Bitcoin prices, high energy costs and fierce completion among miners have depressed the prices of the hardware. The strategy is to buy mining rigs at a steep discount from distressed miners and expand operations at a low cost. Large-scale miner Bitdeer launched a $250 million Bitcoin mining distressed fund last week, while public mining firm CleanSpark Inc. bought a Georgia mining facility and thousands of rigs from another miner for over $30 million.

...

Foundry Digital, which shares the same parent, Digital Currency Group, with Grayscale, will run the mining operations. The Rochester, New York-based company is one of the major crypto-mining services providers. It has the largest Bitcoin mining pool by computing power in the world, according to data from btc.com."

Katherine Greifeld continues th3e GBTC saga in World’s Biggest Crypto Fund Hits Record 42% Discount to Value of Bitcoin It Holds:

"The $11.4 billion Grayscale Bitcoin Trust (ticker GBTC) has plunged more than 74% this year, outpacing the cryptocurrency’s 64% decline. That gap has widened dramatically over the past week, dragging the price of GBTC to an unprecedented 42% discount to the value of the Bitcoin it holds, according to Bloomberg data.

The dislocation is rooted in the fact that despite Grayscale’s best efforts, US regulators have repeatedly denied applications to convert GBTC into a physically-backed exchange-traded fund -- a structure that the Securities and Exchange Commission has yet to approve, despite allowing the futures-backed ProShares Bitcoin Strategy ETF (BITO) to launch a year ago. In its structure as a trust, GBTC isn’t able to redeem shares to keep pace with shifting demand, exacerbating its net-asset value discount while the derivatives-backed ETFs stay in lockstep with theirs."

As Matt Levine explained, HODL-ing BTC is a bad idea compared to using derivatives to track BTC. BITO does this and is only down 65% for the year, the same as BTC.

Katherine Greifeld reports that Grayscale Considers Tender Offer for Bitcoin Trust Fund If SEC Lawsuit Fails:

"A tender offer for up to 20% of the outstanding shares of the $10.7 billion Grayscale Bitcoin Trust (ticker GBTC) is one of the options that the digital asset manager is considering, Grayscale Chief Executive Officer Michael Sonnenshein wrote in a letter to investors Monday. That process, in which Grayscale would ask shareholders to sell back their GBTC shares at an agreed price, would require approval from the Securities and Exchange Commission that the agency “may not provide,” Sonnenshein wrote.

GBTC closed nearly 50% below the value of its underlying Bitcoin on Friday, Bloomberg data show."

Katherine Greifeld and Vildana Hajric report that Valkyrie Unveils Proposal for Grayscale’s Troubled Bitcoin Trust (GBTC):

"Valkyrie Investments is out with a proposal for a much larger rival product: to become the new sponsor and manager of the crypto industry’s largest fund, the Grayscale Bitcoin trust.

The Nashville, Tennessee-based asset manager, which oversees roughly $180 million, on Friday announced the launch of the Valkyrie Opportunistic Fund, which seeks to take advantage of the massive discount in Grayscale Investments’ $10.5 billion product (GBTC). The Valkyrie fund will be increasing its holdings of GBTC, allowing the company to realize “the true value of the underlying Bitcoin for our investors,” which it says is a goal it will actively pursue on their behalf, according to the company."

Good luck with that! It isn't like Grayscale isn't actively pursuing realizing “the true value of the underlying Bitcoin ". It is that the SEC won't let them.

Yevgeniy Feldman's Does Grayscale Have a Future? is an interesting look at the legal issues around GBTC and the SEC's Rule 144.

Matt Levine has another of his excellent explainers in FTX Wants Its Bitcoins Back From Grayscale. There are now two lawsuits about the future of Bitcoin's Hotel California, one where Grayscale is suing the SEC, and one where FTX is suing Grayscale:

"1. Grayscale will either win or lose its lawsuit to convert the trusts into ETFs.

2. If it wins, it will convert them into ETFs, the discount will vanish, FTX/Alameda will be able to redeem or sell at close to net asset value, and FTX’s lawsuit is irrelevant.

3. If it loses, Grayscale really does kind of have to do something? You can’t keep those Bitcoins locked up forever charging 2%."

Post a Comment