Although the

first Non-Fungible Token was minted in 2014, it wasn't until

Cryptokitties bought the Ethereum blockchain to its knees in December 2017 that NFTs attracted attention. But then they were swiftly hailed as the revolutionary technology that would usher in Web 3, the Holy Grail of VCs, speculators and the major content industries because it would be a completely financialized Web. Approaching 5 years later, it is time to ask "how's it going?"

Below the fold I look at the details, but the TL;DR is "not so great"; NFTs as the basis for a financialized Web have six main problems:

- Technical: the technology doesn't actually do what people think it does.

- Legal: there is no legal basis for the "rights" NFTs claim to represent.

- Regulatory: much of the business of creating and selling NFTs appears to violate securities law.

- Marketing: the ordinary consumers who would pay for a financialized Web absolutely hate the idea.

- Financial: like cryptocurrencies, the fundamental attraction of NFTs is "number go up". And much of the trading in NTFs was Making Sure "Number Go Up". But, alas "number go down", at least partly because of problem #4.

- Criminal: vulnerabilities in the NFT ecosystem provide a bonanza for thieves.

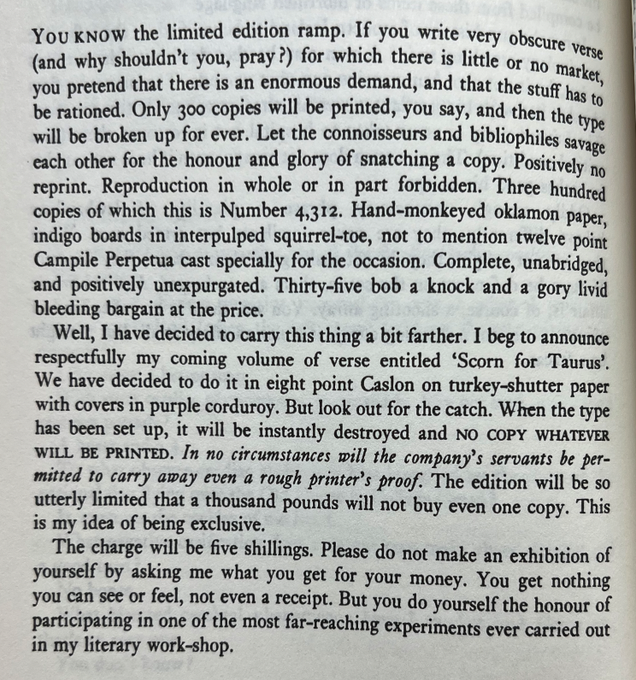

P Nielsen Hayden (@pnh) tweeted

"1942. Flann O'Brien invents the NFT". O'Brien wrote:

You get nothing you can see or feel, not even a receipt. But you do yourself the honour of participating in one of the most far-reaching experiments ever carried out in my literary work-shop.

Alas, Flann O'Brien was ahead of 1942's technology. For the real story of the early history of NFTs you should consult

David Gerard and

Amy Castor. Here I am just going to discuss each of the problems that emerged once people started using the technology.

Technical

The technical problem is that the connection between an NFT and the resource it purports to represent is tenuous in the extreme, as Moxie Marlinspike

brilliantly demonstrated (both links point to the

same NFT) in

My first impressions of web3. I explain the problem in detail in

NFTs and Web Archiving but the brief version is:

the purchaser of an NFT is buying a supposedly immutable, non-fungible object that points to a URI pointing to another URI. In practice both are typically URLs. The token provides no assurance that either of these links resolves to content, or that the content they resolve to at any later time is what the purchaser believed at the time of purchase.

Ownership of a non-fungible real-world object, say a house, confers the right to control access to it. So it was natural that NFT owners would expect the same right. They were disappointed, which led to loud complaints about

"right-clicker mentality among the uninitiated:

what is the “right-clicker mentality”? Quite literally, it is referring to one’s ability to right-click on any image they see online to bring up a menu and select the “save” option in order to save a copy of the image to their device. In this term we have a microcosm of the entire philosophical debate surrounding NFTs.

Another thing

Marlinspike documented is that almost all NFT marketplaces, wallets and associated services don't use the underlying blockchain directly, but only via a couple of API services (Infura and Alchemy). Thus there will always be a centralized service between you and whatever your NFT is supposed to do. An example of this fragility of the connection between an NFT and the resource it purports to represent is Molly White's

Unstoppable Domains disables .coin extensions, illustrating an issue with the idea that "you'll always own your NFT":

Unstoppable Domains is in the business of selling "domains" — at least that's what they call them, but they're not the kind of domain that you can plug into your web browser. Instead, they are more like the ENS domains that you have may have seen (the ones ending in .eth), and they typically map to a crypto wallet address. The organization just discovered that they were not the first to go around selling .coin "domains" (represented by NFTs), and were at risk of running into collisions. As a result, they decided to no longer sell these domains, and stop their libraries and services from resolving them.

But fear not, they said, because "Unstoppable domains are self-custodied NFTs, so you still own your .coin domain, but it won’t work with our resolution services or integrations."

That's right, folks, you'll still have your .coin NFT! It just won't resolve, or be otherwise useful in any way.

The token on the blockchain provides no control over either of the URLs, so it isn't able to fulfill reasonable expectations for the result of purchasing it.

Legal

I wrote in

NFTs and Web Archiving:

There is no guarantee that the creator of the NFT had any copyright in, or other rights to, the content to which either of the links resolves at any particular time.

In December 2020 it became possible for anyone to mint and sell an NFT for real money, when OpenSea announced that

"any user can mint NFTs on its platform for free". At first, OpenSea tried to approve these mints, but in March 2021 they gave up trying and plagiarism erupted. People rushed to mint and sell an NFT of any random image they found on the Web. The

DeviantArt online art community was a

prime victim:

"At DeviantArt, we’ve seen our users suffer at the hands of bad actors in Web3 through art infringement and theft, instead of enjoying the promise and opportunity that Web3 holds for creators," CEO Moti Levy said.

"Artists are doubly punished, first through the theft of their work, and then again by having to file endless DMCA reports to multiple NFT marketplaces," Levy added.

Note that the DMCA notice to the marketplace merely prevents that marketplace offering the plagiarized NFT for sale. Immutability means that the NFT cannot be removed from the blockchain. As usual in technology markets only a few markets dominate the NFT market. So the fact that none of them allow it to appear effectively renders it worthless.

The plagiarism problem got so bad that DeviantArt developed an automated system for detecting and DMCA-ing plagiarized NFTs, as Nica Osorio reports in

DeviantArt Amps Up War On Art, NFT Theft And Infringement With Protect Protocol:

The team launched the DeviantArt Protect in August 2021 which indexes nine blockchains and so far has processed nearly 330,000 Non-Fungible Token (NFT) infringement claims and indexed more than 400 million.

|

| Now "worth" $280 |

Despite this, the problem was so unmanageable that

some markets just gave up:

Cent, the NFT marketplace which sold Jack Dorsey's NFT of his first tweet for $2.9 million, stopped transactions on February 6. The founder explained that people selling NFTs of content they didn't own, copies of other NFT projects, and NFTs resembling securities were "rampant" problems on the platform. "We would ban offending accounts but it was like we're playing a game of whack-a-mole... Every time we would ban one, another one would come up, or three more would come up."

In

NFTs and the One Precedent-setting Law Case That Can Make or Break Them by Dario Garcia Giner argues that NFTs could improve the market for physical art in two ways:

The first is a guarantee to pay artists (and the original gallerist) royalties on a piece’s resale. The second is to limit the damaging influence of predatory flippers with resale limitations. Currently, this is practically unenforceable in the industry.

...

As a proxy for physical ownership, the NFTs smart contracts could be the repository of re-selling restrictions the buyer agrees to uphold in purchasing a physical piece. The first would be NFT royalty contracts, which guarantee a certain percentage of resale income would flow back to the original beneficiaries. The second would be re-selling restrictions, which have already been discussed in the context of tying NFTs to luxury goods.

This could make the NFT the sole channel for all sales past, present, and future.

This is all typical crypto-bro touting

potential benefits. Absent a legal framework recognizing NFTs as being legal contracts conferring rights and duties, this is all so much hot air. And given the problems of NFTs I'm outlining, and their underlying pseudonymity, courts should be very reluctant to recognize them in this way.

Regulatory

Bored-Ape Creator Yuga Labs Faces SEC Probe Over Unregistered Offerings by Matt Robinson illustrates the regulatory risks of NFTs:

The SEC is examining whether certain nonfungible tokens from the Miami-based company are more akin to stocks and should follow the same disclosure rules, according to a person familiar with the matter, who asked not to be named because the probe is private. Wall Street’s main regulator is also examining the distribution of ApeCoin, which was given to holders of Bored Ape Yacht Club and related NFTs. The cryptocurrency was created in part for web3, a vision of a decentralized internet built around blockchains.

...

ApeCoin gives holders influence over another crypto-native entity known as a decentralized autonomous organization, or DAO. The idea was to give the Bored Ape community a hand in shaping the decentralized, blockchain-powered vision of the internet that venture capitalists often describe as web3. The Bored Ape DAO will use the blockchain to enable and record votes on decisions related to how the community is managed.

Voting to govern a token in the hope of making a return on investing in it is pretty clearly equivalent to an equity investment, as Amy Castor's

Bored Apes Yacht Club launches Apecoin. It looks like an unregistered penny stock offering pointed out in March when ApeCoin launched.

This isn't the only regulatory problem for NFTs. In regulated markets wash trading is illegal, but as I wrote in

Making Sure "Number Go Up" it is endemic in cryptocurrency markets and NFTs are no exception. The most notorious example was detailed in Nick Baker's

An NFT Just Sold for $532 Million, But Didn’t Really Sell at All:

The process started Thursday at 6:13 p.m. New York time, when someone using an Ethereum address beginning with 0xef76 transferred the CryptoPunk to an address starting with 0x8e39.

About an hour and a half later, 0x8e39 sold the NFT to an address starting with 0x9b5a for 124,457 Ether -- equal to $532 million -- all of it borrowed from three sources, primarily Compound.

To pay for the trade, the buyer shipped the Ether tokens to the CryptoPunk’s smart contract, which transferred them to the seller -- normal stuff, a buyer settling up with a seller. But the seller then sent the 124,457 Ether back to the buyer, who repaid the loans.

And then the last step: the avatar was given back to the original address, 0xef76, and offered up for sale again for 250,000 Ether, or more than $1 billion.

Marketing

While the idea of a financialized Web is catnip for VCs, speculators and content industries such as game publishers,

those who don't know history are doomed to repeat it. We have been down this path before, the last time with the idea of

micropayments. They were all the rage in the late 90s, but in 2000

Clay Shirky wrote:

The Short Answer for Why Micropayments Fail

Users hate them.

...

Why does it matter that users hate micropayments? Because users are the ones with the money, and micropayments do not take user preferences into account.

Three years later Andrew Odlyzko provided a more detailed analysis of the failure in

The Case Against Micropayments. Now, Brian Feldman recounts how this played out 22 years later in

How Gamers Beat NFTs:

for the better part of the past year and a half, a whole lot of people in the games business thought NFTs sounded great. With crypto booming in the summer of 2021, NFT backers grew beyond the Bitcoin faithful to include Mark Zuckerberg’s Meta, the traditional financial industry, and a string of game publishers whose market values range from modest (Team17, about $700 million) to massive (the crypto-curious Square Enix, $5.2 billion). With games, the idea, broadly speaking, was to merge the well-established, wildly profitable act of selling digital items and the buzzy world of web3, the catchall term for a hazy mix of blockchain, cryptocurrency, and virtual-reality technologies that always seem to be over the next horizon.

So how did these

dreams of avarice work out?

Gamers and industry types have waged a war of public opinion online, dismissing NFT advocates as hucksters, vowing boycotts, and generally making a scene. Protests unraveled or headed off the addition of NFTs or blockchain initiatives by Valve’s Steam marketplace, which has since banned blockchain tech; Stalker2, the Chernobyl disaster sequel; the serial-killer-vs.-survivors game Dead by Daylight; voice actor Troy Baker; Electronic Arts and Sega, which both walked back initial stated interest in NFTs; Discord, the standard chat app for gamers; and, in late July, the Microsoft-owned juggernaut Minecraft. “The initial backlash from consumers was a response to the shallow game mechanics and Ponzi-scheme-like practices that informed most of the early designs,” says Joost van Dreunen, a games industry analyst and investor who teaches about the business of video games at New York University. “It isn’t fun or sustainable.”

It wasn't just gamers who hated NFTs, as

David Gerard reports:

In July 2021, CNN announced with great fanfare its plan for NFTs for News! “Vault is a Web3 project by CNN to reflect on the world events we experience together. Collect NFTs of historic artistic interpretations from digital artists.” Anyway, they’ve just shut it down. [CNN Vault, archive; Twitter]

People who spent actual money on CNN NFTs are yelling that they’ve been rugpulled. Press Gazette estimated that CNN had taken in at least $329,700 by April 2022. CNN was actively promoting spending your money at Vault up to a few weeks before the shutdown. [Press Gazette; The Verge]

CNN claim Vault was just an “experiment.” This doesn’t really match up with the detailed project roadmap they published, which extends into 2023 with a “globe” icon. [CNN, archive]

Vault was running on Dapper Labs’ Flow blockchain. CNN has offered a refund of 20% of minting price — why only 20%? — in USDC stablecoins or FLOW tokens. Flow limits stablecoin withdrawals to $10 per transaction, with a $4 transaction fee. [The Block]

Financial

Another fundamental problem with NFTs is that, because they don't actually control the resource they purport to represent, they don't provide any way to extract rent from it. Thus they cannot generate income, their value is entirely speculative, based on the

Greater Fool Theory. It turned out that, given the prevalence of wash trading, most of the greater fools were the original purchaser themselves. In actual arms-length trades, the fools were definitely lesser. Pranshu Verma's

They spent a fortune on pictures of apes and cats. Do they regret it? provides many examples:

An NFT of Twitter founder Jack Dorsey’s first tweet, purchased last year by an Iranian crypto investor for $2.9 million, was put up for auction in April, with bids topping out at $280. A token of a pixelated man with sunglasses and hat that sold for roughly $1 million seven months ago brought just $138,000 on May 8. A digital token of an ape with a red hat, sleeveless T-shirt and multicolored grin — part of the popular Bored Ape Yacht Club — purchased for over $520,000 on April 30, was sold for roughly half that price 10 days later.

Hayes Brown explains the excess of lesser fools in

NFTs are plunging in popularity? Yeah, that makes sense:

NFTs and cryptocurrency depend on two things to keep their valuations high: increasing demand and perceived scarcity.

Which leads us to two problems the market is facing. First, the number of active traders has plummeted from almost a million accounts at the start of the year to about 491,000, NBC News reported Thursday. A lack of new interest or sustained interest in an asset is rarely a good sign for its longevity.

Second, there’s been a flood of supply. “There are about five NFTs for every buyer, according to data from analytics firm Chainalysis,” the Journal reported. “As of the end of April, there have been 9.2 million NFTs sold, which were bought by 1.8 million people, the firm said.”

That excess supply makes sense when you consider that everyone and their mother have been rushing to pump out an NFT in a bid to get in on the trend.

The result is evident in Sidhartha Shukla's

NFT Trading Volumes Collapse 97% From January Peak:

Trading volumes in nonfungible tokens -- digital art and collectibles recorded on blockchains -- have tumbled 97% from a record high in January this year. They slid to just $466 million in September from $17 billion at the start of 2022, according to data from Dune Analytics. The fading NFT mania is part of a wider, $2 trillion wipeout in the crypto sector as rapidly tightening monetary policy starves speculative assets of investment flows.

Amy Castor's

The NFT market hasn’t crashed — it was never not crashed stresses the lack of a real NFT market:

NFTs are illiquid assets. It’s not easy to find a new sucker everyday willing to pay millions of dollars for a JPEG — not even a JPEG, but a token on a blockchain that points to a JPEG.

This is why we see situations like the one on Feb. 8, when a seller going by @0x650d on Twitter decided to “hodl” his collection of 104 CryptoPunks at the last minute. The collection was supposed to fetch $30 million at Sotheby’s — but there were no buyers.

If you accept that the NFT market is crashing, you have to accept that the NFT market ever existed at all.

The problem with NFT data is that most of it is coming from the NFT platforms themselves. There’s no way to confirm if what they are reporting is real. And there is good reason to suspect the secondary market doesn’t exist at all — it’s just wash trading, meaning the same money is going back and forth between the same people, to pump up the prices.

Most of the activity on LooksRare, a marketplace that launched in January and went on to challenge power player OpenSea, turned out to be fake. In February, Chainalysis reported “significant” wash trading on NFT platforms. Their findings made international news. On May 4, the first day that Coinbase opened its NFT marketplace to the public, the platform had barely any users. This was after Coinbase boasted that 4 million were on the waitlist.

The crashing prices called for creativity among NFT vendors. Molly White's

Former footballer Michael Owen claims his NFTs "will be the first ever that can't lose their initial value" is an example:

In what almost guarantees some fun lawsuits down the line, former footballer Michael Owen tried to hit back at "the critics" by announcing that "[his] NFTs will be the first ever that can’t lose their initial value". Owen's business partner quickly turned up to do damage control, writing "we cannot guarantee or say that you cannot lose. There is always a chance".

It appeared that Owen might have meant that there would be a lower bound on resale price of the NFTs, which is neither a new concept in NFTs (see Kaiju Kongz or Rich Bulls Club), nor does it mean the NFTs "can't lose their initial value". It just means that when the NFTs do lose their initial value, collectors can't recoup even a portion of their investment.

The buyers were equally inventive. If you ever doubted that NFTs were only about "number go up", Molly White's

NFT trading fantasy league emerges to provide traders with the "sweet adrenaline" of flipping NFTs that they're missing in the bear market should set your mind at ease:

"Most of us are too poor to be spending the [ether] we have left on huge sweeps, but we still want that sweet adrenaline rush of flipping JPEGs" said Brian Krogsgard, co-founder of the Flip NFT platform, in a statement you would think might have raised a red flag or two in his own mind. Evidently NFT traders are now being pitched NFT trading fantasy leagues, where they will be able to paper trade NFTs without risking their real-life fake money. Unfortunately for the traders, the app uses actual NFT price data, so the huge NFT project bull runs that some traders experienced during the NFT mania of 2021 will likely not emerge here, either.

Criminal

One fundamental problem with the idea that "you will always own your NFT" is that it is only true while your private key is secret, and even then if you only use it to sign trustworthy transactions. Neither of these is easy to maintain. Here is

Matt Levine on the Bored Ape Yacht Club:

The best and most valuable NFTs offer their owners real social benefits; owning an NFT in a popular series like CryptoPunks or Meebits gives you a sense of community, perhaps some intellectual-property rights, and a way to socialize with like-minded, uh, venture capitalists.

Owning an NFT in the Bored Ape Yacht Club series gives you a particularly valuable social experience: You get to have your Bored Ape stolen and then complain about it online, which lets you feel a sense of kinship with Seth Green and a bunch of venture capitalists who have also had their Bored Apes stolen.

He is right that the BAYC NFTs are likely to get stolen. Molly White documents the second example in two months in

Bored Apes Discord compromised again, 32 NFTs stolen and flipped for $360,000:

Scammers were able to compromise the Discord account of a Bored Apes community manager, then use it to post an announcement of an "exclusive giveaway" to anyone who held a Bored Ape, Mutant Ape, or Otherside NFT. When users went to mint their free NFT, the scammers were able to steal their pricey NFTs. The scammer quickly flipped the stolen NFTs for a total of around 200 ETH (about $360,000), then began transferring funds to Tornado Cash.

Matt Levine continues:

Yeah one lesson here is that there is absolutely no link that the members of the BAYC Discord server won’t click. They just love clicking links! “Maybe this is the link that will get my ape stolen,” they hope, and this weekend they were right.

Look, this is what Bored Ape Yacht Club is! Bored Ape Yacht Club is a way to spend a lot of money to become the victim of an online theft that you can then complain about! You are not getting some other utility from pretending to own a picture of a monkey! But once it is stolen you can commiserate with Seth Green or whatever.

David Yaffe-Bellany is less sarcastic in

Thefts, Fraud and Lawsuits at the World’s Biggest NFT Marketplace:

Mr. Chapman bought the nonfungible token last year, as a widely hyped series of digital collectibles called the Bored Ape Yacht Club became a phenomenon. In December, he listed his Bored Ape for sale on OpenSea, the largest NFT marketplace, setting the price at about $1 million. Two months later, as he got ready to take his daughters to the zoo, OpenSea sent him a notification: The ape had been sold for roughly $300,000.

...

In February, Eli Shapira, a former tech executive, clicked on a link that he said gave a hacker access to the digital wallet where he stores his NFTs. The thief sold two of Mr. Shapira’s most valuable NFTs on OpenSea for a total of more than $100,000.

Within hours, Mr. Shapira contacted OpenSea to report the hack. But the company never took action, he said. Since then, he has used public data to track the account that seized his NFTs and has seen the hacker sell other images on OpenSea, possibly from more thefts.

In

All Their Apes Gone, Nitish Pahwa collected a long list of techniques for stealing Bored Apes NFTs, starting with the now notorious tweet from Todd Kramer. He writes:

I’ve assembled a lengthy, though surely incomplete, list of stolen apes and related scams. (Keep in mind that ape thefts alone are only a fraction all NFT and crypto thefts over time. It’s an expansive universe! Of scams!)

"It’s an expansive universe! Of scams!" really sums it up nicely.

In All Their Apes Gone, Nitish Pahwa collected a long list of techniques for stealing Bored Apes NFTs, starting with the now notorious tweet from Todd Kramer. He writes:

In All Their Apes Gone, Nitish Pahwa collected a long list of techniques for stealing Bored Apes NFTs, starting with the now notorious tweet from Todd Kramer. He writes:

13 comments:

Molly White's Web3 is Going Just Great is full of examples showing the difficulty of maintaining the secrecy of private keys, upon which the whole of the cryptocurrency ecosystem depends. Here are some recent ones:

1. Rubic exchange private key compromised, token plummets.

2. QANX Bridge suffers $1.16 million loss caused by the Profanity vanity address vulnerability.

3. Vulnerability discovered in vanity wallet generator puts millions of dollars at risk.

In NFT vending machine gets cold London reception, Tanzeel Akhtar reports that:

"A neon purple vending machine dispensing nonfungible tokens for £10 ($11.18) a pop has materialized in the middle of London, drawing frosty stares from passers-by in the British capital.

The glowing gadget is the 21st-century iteration of the first coin-operated machines seen in the city in the 1880s, doling out postcards. Sited at the Queen Elizabeth II Centre in Westminster, it will be available between Nov. 3-4 for the NFT.London conference, which brings together the local crypto community for debates and workshops."

UK Parliament Group Starts NFT Inquiry as Crypto Scrutiny Grows by Tanzeel Akhtar starts:

"The UK parliament started an inquiry into nonfungible tokens, the digital collectibles for which Prime Minister Rishi Sunak has been a champion.

The Digital, Culture, Media & Sport committee in the House of Commons announced the initiative in a statement on Friday, adding that it will also study the wider blockchain technology that underpins NFTs.

“MPs are expected to consider whether NFT investors, especially vulnerable speculators, are put at risk by the market,” the DCMS committee said in the statement."

Jason Schreier's Blockchain Game Studio Cuts 10% Of Staff Amid Downturn reports on "widespread disinterest":

"Mythical Games, a blockchain video game company that has raised more than $270 million in venture capital, laid off 10% of its staff and lost three top executives this week.

The layoffs at a company once valued at $1.25 billion are reflective of widespread disinterest in so-called play-to-earn video games, which promise players the opportunity to buy and sell in-game goods for real-life cash using blockchain and nonfungible tokens."

Edward Helmore reports on an innovative new use case for NFTs in Investors convert ‘totally worthless’ NFTs into tax write-offs:

"A recently launched service, Unsellable, aims to help collectors do exactly that. Think of it as a distressed asset fire sale.

“While every investment class has its losers, many of the NFTs we invested in were not only down big; they were now totally worthless … illiquid … unsellable,” the service says on its website.

Unsellable – which says it is “building the world’s largest collection of worthless NFTs” – buys the underlying tokens for a fraction of their original price and provides an official receipt for tax purposes.

Launched a month ago, Unsellable now has 5,000 NFTs, and founder Skyler Hallgren expects that to grow to 15,000 by the end of the month."

It isn't just NFTs. Muyao Shen reports that DeFi Used to Be Crypto’s Hottest Sector. Now It’s Facing a Big Downturn:

"DeFi trading volume has more than halved; the total value of crypto tokens locked in DeFi protocols has been mostly flat for months; and DeFi’s once lofty returns are nowhere to be found. Investors both at the retail and institutional level are less willing to look past security risks and regulatory uncertainty. And with solutions to those problems still years away, a number of DeFi projects may not survive the downturn."

Naturally, the boosters trot out the usual excuse:

'“One thing that’s hard for people to internalize is the timing of new markets and just how long it usually takes for great products to be built on new technology,” said Antonio Juliano, founder and CEO of decentralized exchange dYdX. “That’s actually the root cause of a lot of this boom and bust cycle that we see in crypto.”'

Matthew S. Smith recounts a similar bubble in The Spectacular Collapse of CryptoKitties, the First Big Blockchain Game:

"Although CryptoKitties’ demands on the network subsided as players left, gas will likely be the final nail in the game’s coffin. The median price of a CryptoKitty in the past three months is about 0.04 ether, or $40 to $50, which is often less than the gas required to complete the transaction. Even those who want to casually own and breed inexpensive CryptoKitties for fun can’t do it without spending hundreds of dollars."

This idea lasted a year, not 10 months, but Helen Catt & Sam Francis report that NFT: Plans for Royal Mint produced token dropped:

"Rishi Sunak ordered the creation of a "NFT for Britain" that could be traded online, while chancellor in April 2022.

...

The Royal Mint announced it was "not proceeding with the launch" following a consultation with the Treasury."

Sidhartha Shukla reports that NFT Rout Crushes $1.5 Billion Windfall for Artists as Markets Slash Royalties:

"The friction stems from moves by top NFT exchanges Blur and OpenSea to slash royalty rates payable to artists when a token’s ownership changes, in the hope that lower costs will lift depressed levels of buying and selling.

But diminished artist income could stanch new work, ossifying a market where trading volumes have already crashed 95% from $17 billion in January 2022, according to figures from Token Terminal. Royalties peaked that month at $269 million but were just $4.3 million in July this year as the rates paid fell to 0.6% per transaction from as much as 5%, researcher Nansen said."

Jon Brodkin's Buyers of Bored Ape NFTs sue after digital apes turn out to be bad investment describes the scam:

"The Sotheby's auction house has been named as a defendant in a lawsuit filed by investors who regret buying Bored Ape Yacht Club NFTs that sold for highly inflated prices during the NFT craze in 2021. A Sotheby's auction duped investors by giving the Bored Ape NFTs "an air of legitimacy... to generate investors' interest and hype around the Bored Ape brand," the class-action lawsuit claims.

The boost to Bored Ape NFT prices provided by the auction "was rooted in deception," said the lawsuit filed in US District Court for the Central District of California. It wasn't revealed at the time of the auction that the buyer was the now-disgraced FTX, the lawsuit said.

...

"FTX has several deep ties to Yuga such that it would be mutually beneficial for both Yuga and FTX (as well as Sotheby's) if the BAYC NFT collection were to rise in price and trading volume activity. Upon information and belief, given the extensive financial interests shared by Yuga, Sotheby's and FTX, each knew that FTX was the real buyer of the lot of BAYC NFTs at the Sotheby's auction at the time that Sotheby's representatives were publicly representing that a 'traditional' buyer had made the purchase," the lawsuit said. FTX is not named as a defendant."

Impact Theory to pay $6.1 million for unregistered NFT offering in an SEC first by Molly White reports an SEC success in defining NFTs as unregistered securities:

"Entertainment company Impact Theory has agreed to a $6.1 million payment to settle charges from the SEC that its sales of its "Founder's Keys" NFTs constituted an unregistered crypto asset securities offering. This is the first time the SEC has taken action against issuers of NFTs as unregistered securities offerings."

Olga Kharif and James Tarmy report that NFTs, Once Hyped as the Next Big Thing, Now Face ‘Worst Moment’:

"Nonfungible tokens, most popularly associated with the digital artwork and other collectibles recorded on crypto blockchains, have lost most of their value after once capturing the imagination of crypto enthusiasts as the next big thing. The hype and FOMO, or “fear of missing out,” around NFTs has faded since their all-time peak in January 2022, leaving beaten-down buyers and sellers struggling to find long-term value in the speculative assets.

Monthly trading volume for NFTs plummeted 81% between January 2022 and July 2023, data from DappRadar shows. Over the same period, monthly NFT sales figures have dropped 61%, per DappRadar. And floor prices for blue-chip NFTs like Bored Ape Yacht Club and CryptoPunks are at more than two-year lows, according to industry data tracker NFT Price Floor.

...

Leading NFT marketplace Blur has seen its sales volume — measured in Ether — drop 96% between a late June peak and early August, data from Dune Analytics shows.

The creators behind the digital art have also become concerned after NFT marketplace OpenSea decided to make royalties paid on secondary sales of their work optional, rather than mandatory, last month."

Nick Thompson reports on The People Who Lost Serious Cash on NFTs but remain believers:

"We interviewed five NFT investors – whose losses range from a few thousand quid to $5 million – about what went wrong, what they’re going to do next, and how they feel about the future of NFTs."

Post a Comment