Chris Mellor at

The Register has a

useful update on the evolution of the storage market based on analysis from Aaron Rakers. Below the fold, I have some comments on it. In order to understand them you will need to have read my post

The Medium-Term Prospects for Long-Term Storage Systems from a year ago.

The first thing to note is that the

transition to 3D is proceeding rapidly:

3D NAND bits surpassed 50 per cent of total NAND Flash bits supplied in

2017's third quarter, and are estimated to reach 85 per cent by the end

of 2018,

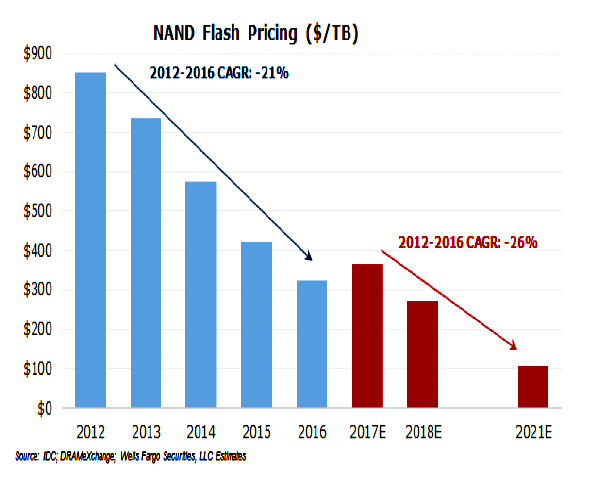

Despite this increase in capacity, price per bit has

increased recently. Rakers' sources all predict that prices will resume their decrease shortly. They didn't predict the increase, so some skepticism is in order. They differ about the

rate of the decrease:

IDC thinks there will be a $/GB decline of 36 per cent year-on-year

2018. TrendForce (DRAMeXchange) recently forecast that 2018 NAND Flash

price declines would be in the 10 to 20 per cent year-on-year range. Western Digital concurs with that from a 3D NAND

viewpoint, and has reported having seen 3D NAND price declines in the 15

- 25 per cent per annum range.

So Rakers' graph is on the

optimistic side, and TrendForce's estimate agrees with

my projection. Rakers projects that SSD's gradual

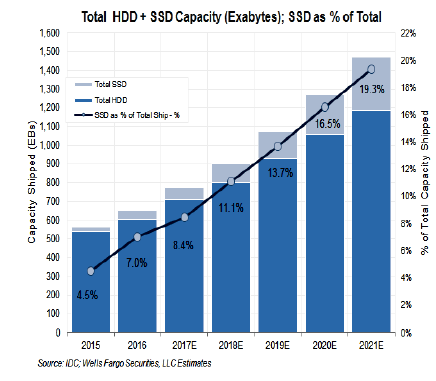

erosion of the hard disk market share will continue:

He looked at SSD ships related to disk drive ships on a capacity basis,

seeing the flash percentage share rising to 19.3 per cent in 2021 from

8.4 per cent this year:

So, as

I projected, Rakers agrees that in 2021 bulk data will still reside overwhelmingly on hard disk, with flash restricted to premium markets that can justify its higher cost.

Mellor ends on a

cautionary note, with which I concur:

It's still not clear if QLC (4bits/cell) flash will actually be an

enterprise-class technology. Flash capacity increases beyond that might

stall because there is nothing beyond QLC, such as a theoretical PLC

(penta level cell - 5bits/cell) technology, or layering beyond 96 x 3D

NAND layers might hit a roadblock.

{kind=link}

{kind=link}

5 comments:

"Moore’s Law has served as a technology metric for storage components for 40+ years. Tape, HDD, and NAND, and Optical technologies are no longer achieving the cost benefits from bit cell scaling relative to Moore’s law expectations. For non-magnetic based technologies planar scaling has moved to 3-D scaling strategies with significant success for NAND structures but with cost/bit deficiencies for Optical. Magnetic based technologies do not have 3-D scaling options. For HDD, 2-D scaling has become problematic with density increase rates significantly below Moore’s law expectation. For Tape, 2-D scaling continues since bit cells are 100X larger in area than HDD bit cells. In sum, both NAND and Tape should provide several generations of storage products that approach Moore’s Law expectations for component capacity and component cost."

This is the conclusion of an invaluable paper by the estimable Robert Fontana and Gary Decad of IBM entitled Moore’s law realities for recording systems and memory storage components: HDD, tape, NAND, and optical. Their cost numbers only go to 2016, so they don't include the recent cost increase for NAND flash. I'm skeptical that NAND will resume a 30%/yr Moore's Law decrease.

The slides from the presentation about the Robert Fontana & Gary Decad paper at the 2017 Library of Congress Storage Architecture meeting are here.

At The Register, Chris Mellor reports on Jim Handy's analysis of XPoint's prospects in the market:

"Incoming persistent memory (PM) technology has a lot of manufacturing cost because it involves new materials and processes, and that makes it more expensive, and this extends the time needed to gain economies of manufacturing scale.

The NAND and NVDIMM-N lessons for XPoint, and other persistent memory technologies aimed at the same DRAM-NAND gap, is that their manufacturing volume needs to be high enough to provide a cost-performance profile matching that of the gap placement on the memory hierarchy chart:"

In other words, prospects don't look good.

"Later this year Micron plans to release quad-level cell flash drives that encroach on the nearline disk drive market. ... QLC flash has a shorter working life than TLC flash and is thought to be more suitable for read-intensive applications, such as long-term stores needing faster access than disk drive-based repositories. ... Samsung, SK Hynix, Toshiba and WDC are also developing QLC flash." reports Chris Mellor at The Register. He concludes:

"We anticipate that all five QLC SSD makers will target the enterprise fast-access, long-term storage market for use cases such as real-time analytics, entertainment and media video asset reuse, and high-value financial data records.

They won't take over the general nearline disk market because disk drives should have a $/GB advantage over QLC SSDs, which will be preserved as new recording technologies such as HAMR and MAMR enable 40TB, and greater, even out to 100TB disk drive capacities."

I'm more pessimistic than Chris about HAMR and MAMR, but I agree that even with QLC's increased bits/wafer there won't be enough of it to displace disk from the bulk storage market.

Remember the Thai floods? The fragility of the storage supply chain is re-emphasized by Anton Shilov at Anandtech:

"A half-hour power outage at Samsung’s fab near Pyeongtaek, South Korea, disrupted production and damaged tens of thousands of processed wafers. Media reports claim that the outage destroyed as much as 3.5% of the global NAND supply for March, which may have an effect on flash memory pricing in the coming weeks."

Post a Comment