|

| Source |

Tether, the largest stablecoin, had a major wobble. Pegged to the U.S. dollar and widely used throughout the cryptocurrency ecosystem, even a fractional cent deviation from its peg can have enormous ramifications. Tether spent six hours below $0.99—at one point slipping down to $0.95—in the most significant deviation from its peg in recent history.

|

| Source |

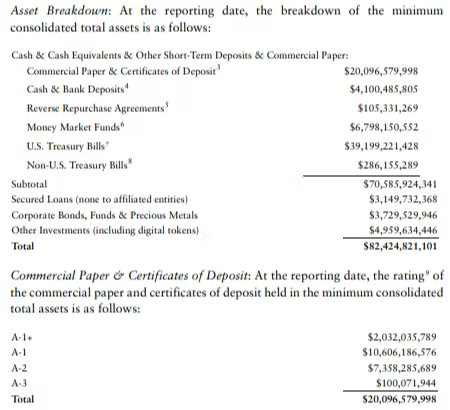

The world’s most popular stablecoin on Thursday posted a letter from MHA Cayman, an offshore outpost of UK mid-tier accountants MHA MacIntyre Hudson, that attests for consolidated total assets of just over $82.4bn. ...Leaving aside the question of how credible these "attestations" are (they are not audits), there remains the question of why anyone would sell their USDT for 95 cents on the dollar?

MHA’s snapshot is from March 31, so it doesn’t capture the USDT coin’s subsequent $8bn drop in market value. It shows less than 5 per cent of reserves in cash, a sum eclipsed even by the mysterious and undefined “other investments” category.

Nevertheless, higher weightings of money-market funds and US Treasury bills meant more than half Tether's total reported assets were in categories considered highly liquid

The explanation starts with this observation from Elder:

Tether’s closed-shop redemption mechanism means it cannot be viewed like a money-market fund. Processing delays can happen without explanation, there’s a 0.1 per cent conversion fee, and the facility is only available to verified customers cashing out at least $100,000.Elder quotes a report from Barclays that takes up the story:

The only way to get immediate access to fiat is to sell the token on an exchange, regardless of the size of holding . . . [W]hile redemption is ‘guaranteed’ at par, the secondary market price of tether can trade lower, depending on the willingness of holders to accept a haircut in return for access to immediate liquidity. As last week’s price action suggests, some investors were willing to accept a nearly 5 per cent discount to liquidate their USDT holdings immediately.Barclays continues:

We think that willingness to absorb losses, even though USDT is fully collateralized and has an overnight liquidity buffer that exceeds most prime funds, suggests the token might be prone pre-emptive runs. Holders with immediate liquidity demands have an incentive (or first-mover advantage) to rush to sell in the secondary market before the supply of tokens from other liquidity-seekers picks up. The fear that USDT might not be able to maintain the peg may drive runs regardless of its actual capacity to support redemptions based on the liquidity of its collateral."pre-emptive runs" are another way of saying metastability. Partly the problem is that, even if you believe the quarterly attestations, they are published after a significant delay. The most recent one was seven weeks out-of-date when it was published. During that time, BTC had fallen from around $47K to around $30K, a 36% drop. Elder writes:

The lack of a realtime view in combination with the short-dated nature of the whole portfolio can raise suspicions about end-of-quarter window dressing.Barclays wraps it up:

All of which makes stablecoins more like ETFs than money-market funds, says Barclays. The issuer is selling a token, after which secondary markets take control. But with ETFs, there is full transparency on the underlying portfolio, which enables market-makers to keep ETF shares trading in line with their benchmark. In the case of stablecoins, market liquidity and sentiment determine how close to realisable net asset value the token will trade

There is, in theory, an arbitrage to be made via the token’s creation and redemption processes. This is analogous to ETFs, which trade around their NAVs, while market makers use the create/redeem processes to maintain prices at levels close to the underlying collateral. Overall, there are several reasons why even this layer of arbitrage may fail, for example, if there are no willing arbitrageurs, if they do not have enough balance sheet to absorb all the selling flows, or if they fear that their requests to redeem will not be honoured in time or in full. Ultimately, full collateralisation helps to reduce stablecoin risk, but does not eliminate it.There are two parts to the problem, even if the backing is more than enough to cover all redemptions:

- Arbitrageurs do not have unlimited capital to devote to maintaining the peg.

- Any delay in redemption consumes arbitrageurs' capital.

The Consolidated Reserves Report alleges assets of $82,424,821,101 and liabilities of $82,262,430,079. This implies approximately $162 million in equity, via standard balance sheet math. You can think of $162 million as the overcollateralization cushion of Tether. If the value of its assets declines by more than $162 million, it requires recapitalization or will, with mathematical certainty, become undercollateralized.

...

The Consolidated Reserves Report alleges that Tether’s reserves included, as of March 2021, $4,959,634,446 of “Other Investments (including digital tokens).” A 3.27% decrease in the value of these investments wipes out all Tether equity and causes their tokens to be undercollateralized.

|

| Source |

even if we believe Tether’s reserves report for the sake of argument, and we grant them very favorable assumptions as to their asset mixes and sagacity as traders, we still arrive at the result that they required recapitalization of the reserves. Their own numbers indict them.An indication that traders share some of McKenzie's skepticism is that, 12 days after Tether dramatically lost its peg, it has continued to trade marginally below $1.

To sum up, metastability is a dynamic process. A static view of the stablecoin's reserves, let alone a static view that is seven weeks out-of-date, is misleading. The only kind of stablecoin that has unlimited, instantaneously available fiat currency backing, and is thus not metastable, is one issued by the central bank, a CBDC.

Non-CBDC stablecoins do not have unlimited, instantaneously available backing, and are thus metastable. Their arbitrage barriers are, in practice, higher than those of algorithmic metastablecoins, but this is a difference of degree only.

10 comments:

Prof. Hilary Allen writes in We’re asking the wrong questions about stablecoins:

"One option that should be on the table is banning stablecoins. This is something we already do with other dangerous products, but hasn’t really been part of this debate so far. Maybe that’s because people believe the decentralisation hype, and think that there’s no way to do it. But given how intermediated stablecoins actually are, there are many points through which a ban could be enforced.

Centralised intermediaries could be banned from issuing stablecoins, and centralised exchanges could be banned from trading them. As for the more decentralised stablecoins and exchanges out there, these are typically operated by “decentralised autonomous organisations” or “DAOs” that act based on votes cast by those who hold governance tokens in them.

Authorities could prohibit anyone from holding governance tokens in any DAO that issues or provides services in connection with a stablecoin. Right now, these governance tokens tend to be concentrated in the hands of founders and venture capital firms. Without VC funding, there’s a good chance that stablecoins would disappear — and that we’d all be a lot better off."

David Gerard and Amy Castor report on the leading metastablecoin:

"The reserve of the allegedly asset-backed stablecoin Tether has, for the first time, dropped by several billion alleged “dollars” in the past month — since the collapse of UST. Tether claimed the reserve held $83 billion on 11 May, but it’s down to $72.5 billion as we write this.

There’s no evidence that $10.5 billion in actual dollars was sent anywhere, or even “$10.5 billion” of cryptos.

We would guess this is first Tether cancelling loans of tethers, in which they printed tethers out of thin air, sent them off to exchanges and accounted the loan itself as the backing asset. This was documented in Tether’s October 2021 settlement with the CFTC, and Celsius just casually told the press they borrowed tethers on this basis as well."

Coindesk has a Freedom of Information suit to make public the composition of Tether's reserves. The New York Supreme Court rejected Tether's attempt to block it a month ago.

David Yaffe-Bellany's The Coin That Could Wreck Crypto looks at Tether:

"Concern is mounting over another potential vulnerability in the crypto market: Tether, a company whose namesake currency is a linchpin of crypto trading worldwide. Long one of the most scrutinized companies in the industry, Tether is facing heightened pressure from regulators, investors, economists and growing legions of skeptics, who argue it could be another domino to fall in an even bigger crash."

Matt Taibbi's The Financial Bubble Era Comes Full Circle is a must-read deep dive into USDC, the #2 "backed" metastablecoin (~$56B vs. USDT ~$66B):

"Trouble started with one question. On April 12, Circle announced it had raised $400 million with investments from BlackRock, Fidelity, Marshall Wace and Fin Capital, noting BlackRock and Circle had entered into a “broader strategic partnership” that would include “exploring capital market applications for USDC” that would “drive the next evolution of Circle’s growth.” This would involve the establishment of a new, BlackRock-managed, government money market fund, the Circle Reserve Fund, through which BlackRock would become “a primary asset manager of USDC cash reserves.”

Sources called with concerns. The fund’s registration statement says “shares are only available for purchase by Circle Internet Financial, LLC.” Not only is this unusual — one legal expert I spoke with said he’d “never seen such a fund… available for sale solely to a single entity” — but it raised a potentially troublesome issue for USDC holders. If Circle is to be the sole counterparty to a reserve fund, that would mean reserves would belong to the company, not its users. This could raise the same issue that recently dogged its partner, the digital exchange Coinbase, when it revealed in an SEC filing that “In the event of a bankruptcy, the crypto assets we hold in custody on behalf of our customers could be subject to bankruptcy proceedings and such customers could be treated as our general unsecured creditors.”

Things get worse from there, so go read on.

Datafinnovation's Circle: A Milder Theory argues that tings aren't as bad as Taibbi suggests:

"Here we offer a far milder theory of what is happening at Circle which does not allege or even suggest any real wrongdoing. It is, perhaps, an intimation some gaming of the system is going on but not in a way that feels outside the bounds of normal business conduct."

In Stablecoins do not make for a stable financial system, Steven Kelley makes an important point about the effect of metastablecoins. Even if they are backed by "safe assets" they have deleterious effects on financial stability:

"The market- and regulation-inspired migration towards safer crypto assets is making stablecoins more popular, but that means there are more investment vehicles gobbling up the safe assets that otherwise grease the wheels of the traditional financial system. Absent rehypothecation, stablecoins will be a giant sucking sound in the financial system: soaking up safe collateral and killing its velocity. A limited supply/velocity of Treasury bills (and Treasury notes/bonds obtained via repos) risks causing collateral shortages, incentivising the creation of private alternatives (which are never really as safe), and putting downward pressure on interest rates. And of course rehypothecation introduces counterparty risks."

Read the whole thing, especially the part about the effects of investors fleeing metastablecoins en masse.

JP Koning asks How profitable is the world's largest stablecoin?:

"So assuming that Ardoino is telling the truth, $13 million in profits over the 12-month period ending March 31, 2022 seems like an accurate estimate to me, given no dividends and the assumption that no capital has been raised.

...

During the period lasting from March 31, 2021 to March 31, 2022, Tether had an average of around 60 billion stablecoins in circulation. That is, Tether's customers had deposited $60 billion with Tether, and Tether had issued its customers 60 billion Tether tokens. The company doesn't pay interest to coin holders, which means it gets to keep all of the income generated by this $60 billion in cash for itself. Assuming an average interest rate of around 0.25% over that period, Tether would have enjoyed interest revenues of around $150 million over those twelve months.

It also would have earned a few million from fees on redemptions and deposits. Each time a customer wants to convert Tether tokens into actual U.S. dollars, they must pay a 0.1% fee.

Out of this $150 million or so in revenue from interest, and another few million from fees, Tether paid expenses such as salaries, court settlements, rent, lawyer fees etc. after which it ended up with $13 million."

Matt Levine returns to writing about Tether:

"The basic situation with Tether is that it claims to be 100% backed by safe assets. Actually it claims to be about 100.3% backed: For every $1 of Tether outstanding, there are about $1.003 of assets that Tether keeps in a box. But Tether is notoriously secretive about what it keeps in the box.

...

And plainly Tether is not always 100%, or 100.3%, backed by very safe assets. For one thing, even its current “reserves breakdown,” as of June 30, 2022, says that 8.36% of its assets are in “Other Investments (Including Digital Tokens),” and digital tokens sometimes lose value. If Tether’s “other investments” lost 10% of their value, then Tether would no longer be fully backed: Each Tether was backed by $1.003 of assets, but if 8% of its portfolio lost 10% of its value then it would be backed by only $0.995 of value. Cryptocurrencies lose 10% of their value all the time."

Suppose Tether isn't really 100% backed?

"The thing that makes a stablecoin worth a dollar is primarily that big crypto investors treat it as being worth a dollar, that they use it as a medium of exchange and a form of collateral and value it at $1 for those uses. Being backed by $1.003 of dollar-denominated safe assets helps with that, but being backed by $0.98 of dollar-denominated assets might be good enough?

One way of putting this might be that Tether is “too big to fail,” that the people who use it have incentives to continue treating it as being worth $1 even if it never to gets around to proving that it has assets worth $1 per Tether."

Frances Coppola's Proof of reserves is proof of nothing is a must-read explanation of "reserves" and what they mean in the cryptosphere, which is nothing like what they mean in banking. It points out the way in which asset-backed metastablecoins such as Tether are subject to the same kind of bank run that took down Silicon Valley Bank.

Post a Comment