My personal experience working with VCs was very positive, but it was (a) a long time ago and (b) they were top-flight firms (Sutter Hill and Sequoia). I've been very skeptical of the current state of the VC industry in

Venture Capital Isn't Working and

Venture Capital Isn't Working: Addendum.

Steven J. Dubner's

Is Venture Capital the Secret Sauce of the American Economy? presents a far more optimistic view, as does

The Economist's

The bright new age of venture capital. On my side of the argument are Fred Wilson's

Seed Rounds At $100mm Post Money and the

Wall St. Journal's

The $900 Billion Cash Pile Inflating Startup Valuations.

Below the fold, some discussion of these opposing views.

Pro

Steven J. Dubner's

Is Venture Capital the Secret Sauce of the American Economy? is a positive view of the contribution of VC-funded companies to the overall US economy. It is based on research published in

Synergizing Ventures by Ufuk Akcigit

et al, who summarize it in

Synergising ventures: The impact of venture capital-backed firms on the aggregate economy:

In a recent paper, we study both empirically and theoretically the role of venture capital (VC) funding – a key source of startup financing – in identifying promising startups and turning them into engines of growth (Akcigit et al. 2019). In particular, we examine the types of startups that get funded by venture capitalists, study the extent to which synergies between venture capitalists and startups and venture capitalist experience matter for firm growth and innovation, and evaluate how critical VC is for growth in the US economy.

|

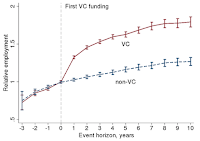

Figure 5

|

They ask whether

VC funding improves a company's outcome:

To assess the magnitude of VC treatment effects, the selection of startups by venture capitalists must be taken into account. To control for selection based on observables, we match VC-funded firms with observationally similar non-funded firms along key dimensions, including year of initial funding, industry, state, age, and employment. Figure 5 plots the evolution of (ln) average employment for VC-funded firms and their matched counterparts over the period spanning three years prior to initial funding to 10 years afterwards. Among firms that patent, Figure 6 plots the evolution of (ln) citation-adjusted patent stock of VC-funded firms and their matched counterparts.

|

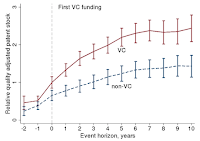

Figure 6

|

The answer isn't a suprise —

VC funding is good for a company:

In both figures, the VC-funded and non-funded groups exhibit virtually identical trajectories before VC funding. However, subsequently VC-funded firms grow and innovate much more. Average employment increases by approximately 475% by the end of the horizon for VC-funded firms, whereas growth is much more modest for the control group (230%). Similarly, the average patent stock of VC-funded firms grows by about 1,100% over the 10-year horizon, as opposed to 440% for the control group. These results suggest that venture capitalists play an important role in the making of successful firms.

It has long been known that there are many mediocre VCs and a few really good ones. Here, for example, is

Bill Janeway's take:

let me just say one thing about venture capital that’s really different. It’s not the extremely skewed returns: we see that across various asset classes. Rather, it’s the persistence of a firm’s returns over several decades, as seen in the US and documented with the data provided not by venture capitalists themselves, but by their limited partners!

|

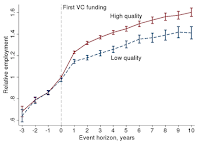

Figure 7

|

Akcigit

et al investigated this effect:

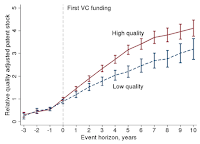

To understand a potential source of these treatment effects, we examine the heterogeneous impact on firm outcomes of being funded by more experienced versus less experienced venture capitalists. To do so, we first divide venture capitalists into two groups. Venture capitalists in the top decile of the ‘total deals’ distribution are labelled as “high quality” (high experience), and the remaining venture capitalists are labelled as “low quality” (low experience). Then, VC-funded firms are separated into those funded by high-quality versus low-quality venture capitalists. Figure 7 plots the evolution of (ln) average employment of firms in each of these categories, and Figure 8 plots the evolution of their (ln) average quality-adjusted patent stock.

|

Figure 8

|

Again, the

result is as expected:

While firms backed by high- and low-quality venture capitalists are similar prior to VC involvement, the average employment and average patent stock of startups funded by high-quality venture capitalists is higher after VC involvement, and the gap between the two groups widens over the 10-year horizon. By the end of the horizon, average employment grows by about 400% in the high-quality group, versus 320% in the low-quality group. Similarly, by the end of the horizon, the average patent stock grows nearly 50-fold for the high-quality group, and only 19-fold for the low-quality group. We confirm that startups funded by high-quality VCs have better employment outcomes through a regression analysis that controls for both startup characteristics and initial funding infusion. These findings suggest that factors beyond funding, such as expertise and management quality associated with high-quality venture capitalists, matter for subsequent firm outcomes.

|

| Source |

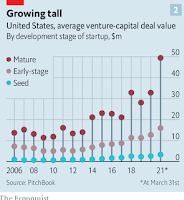

The Economist's

The bright new age of venture capital is a similarly optimistic take:

YOUNG COMPANIES everywhere were preparing for doomsday in March 2020. Sequoia Capital, a large venture-capital (VC) firm, warned of Armageddon; others predicted a “Great Unwinding”. Airbnb and other startups trimmed their workforces in expectation of an economic bloodbath. Yet within months the gloom had lifted and a historic boom had begun. America unleashed huge stimulus; the dominance of tech firms increased as locked-down consumers spent even more of their time online. Many companies, including Airbnb, took advantage of the bullish mood by listing on the stockmarket. The market capitalisation of American VC-backed firms that went public last year amounted to a record $200bn; it is on course to reach $500bn in 2021.

With their pockets full, investors are looking to bet on a new generation of firms. Global venture investment—which ranges from early “seed” funding for firms that are only just getting going to funding for more mature startups—is on track to hit an all-time high of $580bn this year, according to PitchBook, a data provider. That is nearly 50% more than was invested in 2020, and about 20 times that in 2002.

The money isn't just the result of previous successes by the VCs, it is coming from

investors new to the space:

The frenzy is a result of both the entrance of new competitors and greater interest from end-investors. That in turn reflects the fall in interest rates across the rich world, which has pushed investors into riskier but higher-return markets. It has no doubt helped that VC was the highest-performing asset class globally over the past three years, and has performed on a par with bull runs in private equity and public stocks over the past decade.

End-investors who previously avoided VC are now getting involved. In addition to alluring returns, picking out the star funds may be easier for VC than for other types of investment: good performance tends to be more persistent, according to research in the Journal of Financial Economics published last year.

|

| Source |

Increased demand from VCs for deals has had the

inevitable effect:

The rush of capital has pushed up prices. Venture activity for seed-stage startups today are close to those of series A deal sizes (for older companies that may already be generating revenue) a decade ago. The average amount of funding raised in a seed round for an American startup in 2021 is $3.3m, more than five times what it was in 2010

The biggest VC firms, as usual, have

outsized wallets:

The result is that the industry has become more unequal: although the average American VC’s assets under management rose from $220m in 2007 to $280m in 2020, that is skewed by a few big hitters. The median, which is less influenced by such outliers, fell from $70m to $48m. But this is not to say that the industry has become dominated by a few star funds. Market shares are still small. Tiger Global, for instance, led or co-led investments worldwide worth $5bn in 2020, just 1.3% of total venture funding.

...

Company founders, for their part, have gained bargaining power as investors compete. “There’s never been a better time to be an entrepreneur,” says Ali Partovi of Neo, a VC firm based in San Francisco.

Note, for example, Andreeesen Horowitz' $2.2B fund devoted solely to cryptocurrency startups such as Chia.

The Economist notes that the proportion of startups exiting via the preferred route, an IPO, has increased:

The big-tech firms used to gobble up challengers: acquisitions by Amazon, Apple, Facebook, Google and Microsoft rose after 2000 and hit a peak of 74 in 2014. But they have fallen since, to around 60 a year in 2019 and 2020, perhaps owing to a fear of antitrust enforcement (see United States section). More startups are making it to public markets. Listings, rather than acquisitions or sales, now account for about 20% of “exits” by a startup, compared with about 5% five years ago.

Con

First, note that although the rate of acquisitions by the FANGs has dropped, but only from 74 to around 60. On average, they are each buying a company a month. Second, note that acquisitions still outnumber listings by 4 to 1. Third, lets look at how well the companies that did list are doing.

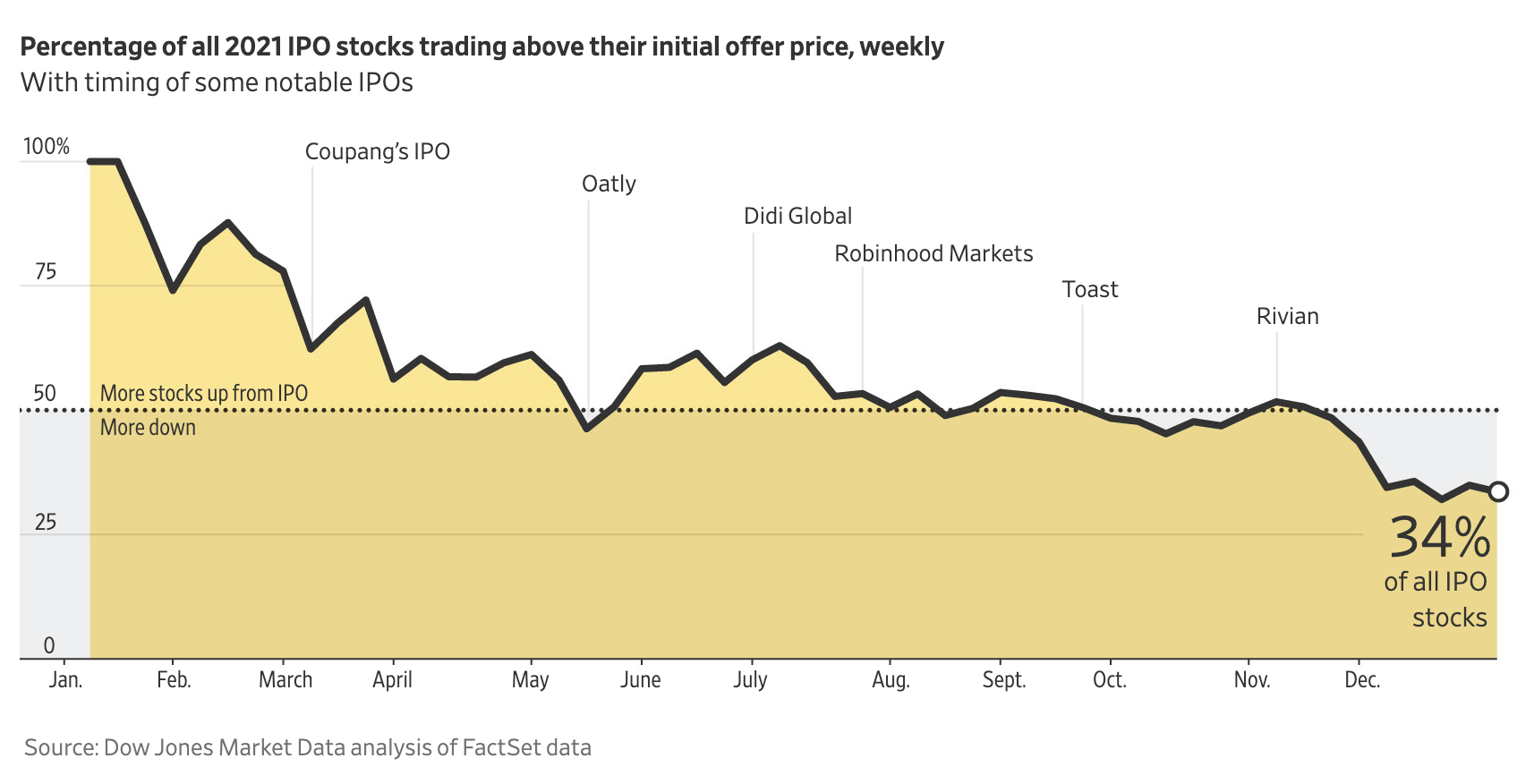

This graph is from a

Wall St. Journal article entitled

IPOs Had a Record 2021. Now They Are Selling Off Like Crazy by

Corrie Driebusch and Peter Santilli:

Looming behind a record-breaking run for IPOs in 2021 is a darker truth: After a selloff in high-growth stocks during the waning days of the year, two-thirds of the companies that went public in the U.S. this year are now trading below their IPO prices.

Although the investors who bought in the IPOs are likely under water, the VCs who sold in the IPOs did well, As

The Economist wrote:

With their pockets full, investors are looking to bet on a new generation of firms.

The

Wall Street Journal focuses on

The $900 Billion Cash Pile Inflating Startup Valuations:

Investors are defying a share-price slump for newly public companies to make hundreds of billions of dollars available to startups, a cash pile that promises to inject a torrent of money into early-stage firms in 2022 and beyond.

Some of this money comes in the

form of a SPAC:

Special-purpose acquisition companies, which take startups public through mergers, raised about $12 billion in each of October and November, roughly doubling their clip from each of the previous three months, Dealogic data show. So far in December, three SPACs a day are being created. While that is below the first quarter’s record pace, it brings the total amount held by the hundreds of SPACs seeking private companies to take public in the next two years to roughly $160 billion.

But most of it still comes from VCs, but with an

increasing proportion from private-equity firms:

The cash committed to venture-capital firms and private-equity firms focused on rapidly growing companies but not yet spent also is ballooning. So-called dry powder hit about $440 billion for venture capitalists and roughly $310 billion for growth-focused PE firms earlier this month, according to Prequin.

Just as the

WSJ headline suggests, startup valuations have become inflated. In

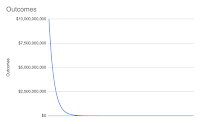

Seed Rounds At $100mm Post Money, Fred Wilson writes "We have been seeing quite a few seed rounds getting done in and around $100mm". He runs the numbers on a hypothetical $100M fund making 100 $1M seed round fundings each getting 1% of the company, for a $100M/company post-money valuation. There are three key parameters of his model:

- 2/3 dilution from seed to exit, so the fund ends up at exit with only 0.3% of the company.

- A 0.75 power-law of returns among the 100 companies, as shown in the graph.

- The best performing among the companies exits at a $10B valuation.

The

result is:

a $100mm seed fund that makes all of its investments at $100mm post-money will barely return the fund. And that number is gross, before fees and carry.

The fund put in $1M and got out $1.333M. That isn't a viable VC fund. Wilson points out that the

valuation is the problem:

f you run that same model with a $20mm post-money value, you get a 6.667x fund before fees and carry. That’s a strong seed fund, probably a tad better than 4x to the LPs, after fees and carry. If you think you can get one of your hundred seed investments to a $10bn outcome, then paying $20mm post-money in seed rounds seems to make a lot of sense.

But Joseph Flaherty tweets that

$10B valuations are rare:

It is important to note that the data underlying Ufuk Akcigit

et al's analysis is entirely from the period before the most recent tsunami of money hit startups. It largely reflects the VC ecosystem back in the days when I worked at startups, with the balance of power in favor of the VCs.

They write:

The analysis is carried out by combining data on all employer businesses in the US from the Census Bureau’s Longitudinal Business Database (LBD), with data on patenting from the USPTO, and deal-level data on firms receiving VC funding from VentureXpert for the period 1980-2012. A key advantage of the data is that it enables us to track the evolution of employment and patenting for all employer businesses in the US, and, critically, differentiate between the experience of VC-funded firms and other firms in the economy.

The current balance of power is in favor of founders like

Travis Kalanick,

Adam Neumann,

Justin Zhu, and

Elizabeth Holmes.

The Economist notes this change:

The shift has also weakened governance. As the balance of power tilts away from them, VCs get fewer board seats and shares are structured so that founders retain voting power. Founders who make poor chief executives—such as Travis Kalanick, the former boss of Uber, a ride-hailing firm—can hang on for longer than they should.

What Akcigit

et al don't investigate is the extent to which their earlier results, showing the beneficial effects of VC funding, are due not to the overall effect of VC funding, but to the large effect of high-quality VC funding on a small proportion of the funded companies. Nor do they investigate whether the effect of the more recent flood of money, the resulting proliferation of VCs, and the shift in the balance of power toward founders, has resulted in the small proportion of companies funded by high-quality VCs has become even smaller, thus dragging down the aggregate benefit of VC funding to the economy.

As I wrote in

Venture Capital Isn't Working:

I'm a big believer in Bill Joy's Law of Startups — "success is inversely proportional to the amount of money you have". Too much money allows hard decisions to be put off. Taking hard decisions promptly is key to "fail fast".

"Fail fast" used to be the mantra in Silicon Valley. In most of the world success was great, failure was bad, not doing either was OK. In Silicon Valley success was great, failure was OK, and not doing either was a big problem. Trying something and failing fast meant that you had avoided wasting a lot of money and time on an idea that wasn't great, and you had freed up money and time to try something else. Now the mantra seems to be "fake it till you make it", which pretty much guarantees a waste of time and money.

16 comments:

William Janeway weighs in on my side of the debate with Capital Is Not a Strategy:

"investors (both institutional and retail) have become increasingly aggressive in their pursuit of positive real returns. Not only have they accepted increased levels of fundamental risk (that is, the risk of business failures wiping out the value of their securities); they also have become increasingly willing to accept illiquidity, buying securities that they cannot freely resell.

One dramatic example of this phenomenon is the flood of “nontraditional capital” – the National Venture Capital Association’s term for mutual funds, hedge funds, sovereign wealth funds, and so forth – into venture-backed private companies at historically high valuations. Others are the bubbles in crypto assets and the (often fleeting) explosion of “meme” stocks, driven by Reddit communities and retail investors on apps like Robinhood.

Finally, the apparently limitless supply of low-cost capital (in terms of ownership dilution) available to entrepreneurs and early-stage venture-capital firms has had a third-level effect as well: the proliferation of business models with little or no potential to generate sustainable, self-financed growth."

And:

"the extraordinary increase in the supply of capital has eliminated any perceived need for critically assessing business models and business plans, undermining the Golden Rule of venture capital: that those who have the gold set the rules.

Instead, there has been a shift in the balance of power between entrepreneurs and VCs. This is evident in the increased number of start-ups whose founders are entrenched in control no matter how much capital is raised."

More evidence for the "too much money" thesis in Hannah Zhang's Where Did VC Money Go in 2021? Crypto Startups.:

"According to a report published Friday from Galaxy Digital Research, venture capital firms poured $32.8 billion into startups in the crypto and blockchain technology sector, a figure that was higher than all prior years combined. This massive amount of dry powder minted at least 47 companies with valuations above $1 billion — so-called “unicorns” — in the crypto market. In 2021, deal count also stood at an all-time high of more than 2,000, almost twice as many as the year before.

...

In the fourth quarter, the median valuation of crypto and blockchain companies stood at $70 million, more than twice the $29 million valuation seen in other sectors. According to the report, this highlights the “founder-friendly environment and the intense competition among investors for allocation.”

Josh Wolfe of Lux Capital is on my side of the argument too, as Michelle Celarier writes in The Renaissance Man of Venture Capital:

"“The macro is insane,” he says, referring to the market conditions that are outside of the firm’s control and have bid companies up to stratospheric heights in the past few years. “Our main competitive advantage when the market turns — and I’m tracking for signs of when that will be — is our steely fortitude,” he says.

Wolfe mentions that years ago, Lux’s partner meetings, held on Mondays and Thursdays, were full of talk about problems with CEOs or down rounds of financing. “Every meeting right now,” he says, “is, ‘Oh, another one of our companies just went public, a SPAC just bought this company, these guys just got a $300 million offer from Tiger,’” referring to Tiger Global Management, the big hedge fund that is a major VC investor."

Barry Ritholtz reports that:

"According to CBI’s State Of Venture 2021 Report, global venture funding was up 111% in 2021 hitting $620.8B. As the chart above shows, the US accounted for more than half of that, growing 107% in 2021 to reach $311.2B in investments.

...

Not surprisingly, Silicon Valley led the US in VC funding in 2021, with more than $100B invested (Q4’21 was a record $29.3B); New York was 2nd at $65 billion, followed by Boston ($31B), L.A. ($24B), Seattle (~$7B), D.C. (~$5B), and Denver (~$5B). The U.S. led in global exits in 2021, followed by Europe and Asia."

Too much money.

Erin Griffith's ‘It’s All Just Wild’: Tech Start-Ups Reach a New Peak of Froth gives a good idea of the insanity too much money has caused:

"For Daniel Perez, a co-founder of Hinge Health, a provider of online physical therapy programs, the unsolicited emails from investors started in late 2020. They contained pitch decks packed with the elaborate research that the investment firms had done on Hinge, including interviews with dozens of its customers and data on its competitors.

These “reverse pitches,” which numbered in the 20s, were meant to persuade Mr. Perez to take money from the investment firms. He also got several term sheets, or investment contracts, from investors he had never met before."

In What Elizabeth Holmes and Theranos Reveal About Venture Capitalism, Sebastian Mallaby points out that Theranos wasn't actually funded by VCs:

"First, nearly all the money raised by the company came not from venture capitalists but from technology outsiders. The Walton family (which made its fortune from Walmart) invested $150 million. The media baron Rupert Murdoch invested $121 million. The DeVos family (Amway) and the Cox family (radio and television stations), kicked in $100 million each. Apparently, none of these venture tourists bothered to insist on evidence that the Theranos technology worked. By contrast, when Ms. Holmes pitched Theranos to a real venture partnership, MedVenture, she was unable to answer their questions, and the meeting ended with her abrupt departure."

Ryan Breslow's thread Stripe and YCombinator, the Mob Bosses of Silicon Valley (Unroll here) is a must-read expose of the way having too much money allows you to ensure no-one else makes money:

"Stripe and YC have done good things for Silicon Valley.

They’ve provided strong payment APIs to developers who’ve needed it.

And important guidance to founders looking to make it in tech.

But like anyone else with tooooo much power.

Power corrupts."

Jamie Powell is on the "too much money" side of the argument. He writes in Tiger Global: pay and spray:

"Up until Christmas last year, the New York-based fund made 340 unlisted investments, or roughly one a day, according to Nikkei Asia, as it splurged capital at a pace never seen before by those who punt on start-ups."

But "eschewing due diligence" has risks. Powell describes Tiger's investment in BharatPe, which is starting to look like a train-wreck:

"This $2.9bn valuation came just six months after BharatPe was valued at $900m in a funding round led by fellow Tiger-cub Coatue Management. And, perhaps more importantly, after questions had already been raised about BharatPe’s toxic work culture."

Dan Primack has more on the aftermath of Ryan Breslow's thread in Tech founder vs. the "Silicon Valley mob".

The Economist's Buttonwood column How unlisted startups’ valuations will adjust to falling share prices is yet more evidence for the "too much money" thesis:

"An index of stocks that have floated via an initial public offering (IPO) within the past two years, compiled by Renaissance Capital, is down by around a third in the past year. In the private markets where venture capitalists (VCs) supply funding for startups, the term you hear for more sober valuations is “reset”."

But:

"Big new funds are still being raised, even after the repricing of listed tech stocks. VC does not yet seem to have lost any of its sheen with pension funds, endowments and family offices. As long as the money flows in, it will be deployed. The reset may have to wait a while."

Barry Rithotlz interviews Sebastian Mallaby about his new book The Power Law: Venture Capital and the Making of the New Future in his Masters in Business podcast.

Startups bag billions to fill gaps left by chip world giants by Agam Shah reports on how much it takes to do a chip startup these days:

"Software startups have been the darling of VCs, and a lot more money and product planning is needed to put chips into customers' hands, Cerebras Systems CEO Andrew Feldman told The Register.

"It usually costs more than $50m to see the first product in a semiconductor startup," Feldman said. Cerebras has so far raised more than $730m, and was last year valued at more than $4.1 billion.

"From start to first product in a semiconductor company will take an order of three years. As a result, the customer to semiconductor product feedback loop is much longer. VCs don't get feedback for years after they invest capital," Feldman said."

Doomberg's Crouching Tiger, Hidden Problems is a fascinating slow-burn on valuations in private markets that ends up asking:

"We’ve heard the whispers from our friends in the VC sector about the crazy valuations Tiger is paying to close these deals, and one wonders just how much due diligence can be going on when you are doing two deals a day. Perhaps it is just a coincidence that Bloomberg recently reported on Tiger’s rough start to 2022:

“Chase Coleman’s Tiger Global Management posted a 10% decline for its flagship hedge fund last month, a significantly steeper drop than the broader market, according to people familiar with the matter. That follows a 14.8% swoon in January, extending its loss for the year to 23%.”

Most financial crises find their genesis in obscure parts of the markets that fly under the radar until it is too late to stop the contagion. Will the bubble in private market valuations be the catalyst for the next major downturn?"

The boom in SPAC is over. Renaissance Capital posted Special Report: SPAC merger returns crumble, upending the 2022 SPAC market:

"After last year’s SPAC boom, 2022 has started off as a bust. Of the 199 companies that went public via SPAC merger in 2021, only 11% trade above the offer price, and the group averages a -43% return. Completed SPAC mergers (de-SPACs) have performed worse than traditional IPOs, even after a recent sell-off in the IPO market. As of March 2022, de-SPACs have generally underperformed across the board, regardless of SPAC size, year, or target sector. Many of the largest de-SPACs show significant losses, such as Grab and Ginkgo Bioworks. Former high-flyers Virgin Galactic and Hyliion trade below issue, and even high-profile winners Lucid and Draftkings have shed 50% or more over the past few months. Meanwhile, SPACs that have not completed mergers once again trade close to the $10 redemption price, a far better trade relative to de-SPACs."

The FT's Alphaville has two posts on venture capital during the "tech wreck". First A Minsky moment for venture capital?:

"Refinitiv’s venture capital index, which uses the performance of individual VC portfolios and listed stocks to mimic the performance of the broader industry, tanked another 24.2 per cent in April, taking its 2022 loss to a comically bad 45.8 per cent (NB, the Nasdaq is “only” down 19.7 per cent YTD).

That is comfortably its worst monthly performance since worst of the dotcom bust two decades ago.

...

But the danger is that we are on the cusp of what Abraham Thomas earlier this year described as a “Minsky Moment in Venture Capital”, where bad performance reverses investor inflows and both start feeding on each other.

His Substack from February is worth reading to understand how the velocity of funding rounds might produce something like a VC Minsky moment, despite the absence of leverage and liquidity mismatches."

And Tiger is suffering one of the biggest hedge fund drawdowns in history:

"Back of the envelope calculations based on the reported $35bn size of Tiger’s overall public equities book at the end of last year indicate that it has probably suffered a nominal loss of at least $15bn in 2022."

Tiger innovated the "spray and pray" VC strategy:

"In the past two years, Tiger has developed an entirely unique investment platform in venture/growth based on Maximum Deployment Velocity and Better/Faster/Cheaper Capital for Founders."

It worked great until it didn't.

The Tech Rout Isn’t Just Cyclical—It’s Well-Earned, and Overdue by Brad Stone and Lizette Chapman takes my side of the debate:

"The technology industry and its risk-happy patrons have learned, time and again, what happens when short-term profiteering takes precedence over the development of stable companies that can create cool stuff. And yet, here we are again. Years of wildly inflated valuations, crypto-flavored pyramid schemes, and all manner of naked opportunism have led us to the Bust of 2022."

Go read the whole article.

Post a Comment